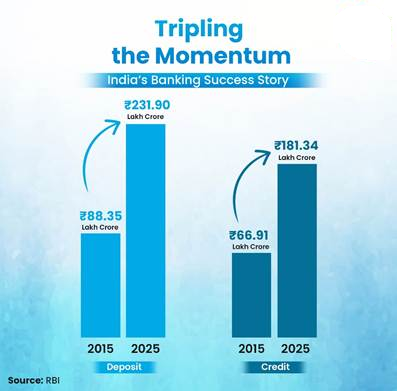

1. Bank deposits and credit (domestic) have nearly tripled between 2015 and 2025, with deposits rising from ₹88.35 lakh crore to ₹231.90 lakh crore and credit expanding from ₹66.91 lakh crore to ₹181.34 lakh crore.

2. Capital buffers have strengthened- the capital to risk weighted assets (CRAR), which measures capital adequacy, rose from 12.94% in March 2015 to 17.36% in March 2025 with CET-1, which represents the highest quality capital a bank can hold, increasing from 9.98% to 14.81% during the same period.

3. Asset quality has also improved. Gross Non-Performing Assets (GNPA) and Net Non-Performing Assets (NNPA) have reduced to 2.2% and 0.5% in March 2025 after rising to highs of 11.18% and 5.94% respectively in March 2018.

4. Profitability of banks has enhanced significantly. Between FYs 17-18 and 24-25, Return on Assets (RoA) increased from -0.22% to 1.37%, and Return on Equity (RoE) jumped from -2.74% to 14.09%.

NPA Decline: An Upward Shift in the Quality

| Section |

Details |

| 1. Understanding NPAs and Their Impact |

Definition: An asset becomes a Non-Performing Asset (NPA) when it stops generating income for the bank.

Impact: Rising NPAs reduce bank profitability because more capital must be allocated to cover bad loans, leading to:

– Credit crunch

– Constrained lending

– Slower economic growth |

| 2. Historical Context (2008–2014) |

Loan Growth: Gross advances of Scheduled Commercial Banks (SCBs) rose from ₹23.34 lakh crore (Mar 2008) to ₹61.01 lakh crore (Mar 2014).

Causes of Rising NPAs:

– Aggressive lending practices

– Willful defaults and loan frauds

– Economic slowdown

Asset Quality by 2014:

– Stressed assets: 9.8% of loan book

– Restructured standard loans: 5.7% |

| 3. Asset Quality Review (AQR) and Peak NPAs (2015–2018) |

AQR 2015: Focused on transparency and full provisioning, revealing higher actual NPAs.

Impact:

– GNPA ratios rose as stressed assets were reclassified as NPAs

– GNPA peaked at 11.46% (₹9,62,621 crore) by March 2018

– Gross NPAs were ₹2,51,054 crore (4.1%) in 2014, rising sharply post-AQR |

| 4. Decline in NPAs (2018–2025) |

Government Measures (“4 Rs”): Recognition, Resolution, Recapitalization, Reforms

Impact:

– Gross NPA ratio declined to 2.79% (₹2,73,413 crore) by March 2025

– Stressed assets including restructured loans reduced from 9.8% (2014) to 3.55% (2025)

Bank Performance:

– GNPA ratio: 2.31% (Mar 2025) – lowest in 20 years

– NNPA ratio: 0.52% (Mar 2025) from 6.1% (2018 peak)

– Strong provision buffers contributed to lower NNPAs |

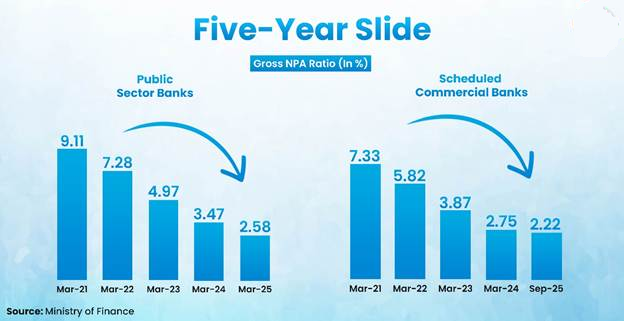

| 5. Public Sector Banks (PSBs) Performance |

Gross NPAs: Declined from 9.11% (Mar 2021) to 2.58% (Mar 2025)

NNPAs: Fell to 0.52% (FY 24-25) from 1.24% (FY 22-23)

Implication: Sustained improvement in asset quality and risk management |

| 6. Key Takeaways |

Structural Improvement: NPAs declined due to transparent recognition, resolution of stressed assets, and strong provisioning.

Robust Banking Health: SCBs and PSBs show strong capital adequacy, improving profitability and lending capacity.

Positive Outlook: Sound macro-economic fundamentals and risk management practices have boosted investor and market confidence |

Bank Profitability on the Rise

The Indian banking industry has seen robust growth, driven by strong economic expansion, rising disposable incomes, growing consumerism, and easier credit access. Digital modes of payments, dominated by UPI, have grown by leaps and bounds over the last few years. As per the RBI, India’s banking sector is sufficiently capitalized and well-regulated. Notably, profitability of banks improved for the sixth consecutive year in 2023-24.

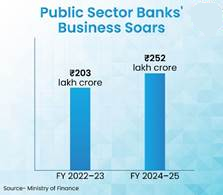

Public Sector Banks

From FY 22–23 to FY 24–25, the total Business of Public Sector Banks (PSBs) rose from ₹203 lakh crore to ₹252 lakh crore

From FY 22–23 to FY 24–25, net profit increased from ₹1.05 lakh crore to ₹1.78 lakh crore.

Dividend payouts grew from ₹20,964 crore to ₹34,990 crore, reflecting the continued strengthening of financial performance.

Scheduled Commercial Banks (SCBs)

During FY 24-25, SCBs recorded their highest ever aggregate net profit of ₹4.01 lakh crore, compared to the net profit of ₹3.5 lakh crore in FY 23-24. The growth trajectory continues, as SCB’s recorded an aggregate net profit of ₹1.02 lakh crore in first 3-months of FY26.

Continuing on this success, the profitability of SCBs improved during FY 25, with Profit After Tax surging by 14.7% (YoY). Gains in profitability continued with Return on Assets (RoA) at 1.37% and Returns on Equity (RoE) at 14.1%.

Besides, banks’ capital position remained satisfactory, as reflected in key parameters like leverage ratio (which measures the proportion of a bank’s Tier 1 capital to its total assets, serving as a safeguard against excessive risk exposure) and capital to risk weighted assets ratio (CRAR), defined as the ratio of total capital funds to risk-weighted assets. The leverage ratio for all SCBs was 7.9% in September 2024 (the range of 6 to 8% is generally considered prudent). PSBs are adequately capitalised, with their CRAR standing at 16.4% as of June 2025.

Strong credit expansion by Non-Banking Financial Companies (NBFCs), that offer services similar to banks, such as loans and investments, but do not possess a full banking license, was accompanied by further strengthening of their balance sheets, improvement in credit quality and profitability, and satisfactory capital buffers.

Factors Propelling Performance of India’s Banks

1. The Asset Quality Review (AQR) launched in 2015 compelled banks to recognize the true state of their loan books, bringing hidden NPAs to light and strengthening the supervisory framework. Additionally, the Government also implemented a comprehensive 4R’s strategy, consisting of recognition of NPAs transparently, resolution and recovery of value from stressed accounts, recapitalizing of PSBs, and reforms in PSBs and the wider financial ecosystem for a responsible and clean system.

2. The Prompt Corrective Action (PCA) framework helped restore the health of weak banks, followed by the consolidation of 27 PSBs into 12 by 2020. A detailed review of business in terms of sustainability, profitability, viability and projections along with credit risk related actions have been beneficial.

3. The Insolvency and Bankruptcy Code (IBC) introduced in 2016, along with complementary out-of-court resolution mechanisms, transformed India’s credit culture and improved recovery processes. It changed the creditor-borrower relationship, taking away control of the defaulting company from promoters/owners and debarred willful defaulters from the resolution process.

4. Sharper recovery laws: Key legislations such as the SARFAESI Act, 2002 (The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002) and the Recovery of Debt and Bankruptcy Act have been amended to enhance their effectiveness in asset recovery.

5. Focused debt resolution: The pecuniary jurisdiction of Debt Recovery Tribunals (DRTs) was raised from ₹10 lakh to ₹20 lakh, enabling them to prioritize higher-value cases and improve recovery efficiency.

6. Specialized recovery mechanisms: PSBs have established dedicated stressed asset management units for close monitoring and faster resolution of NPAs. The deployment of business correspondents and incorporation of a business strategy that uses physical sales and marketing force to interact directly with customers (Feet-on-street model), has further boosted recovery efforts.

In October 2025, the RBI issued a landmark reform through its Draft Directions 2025, proposing a shift to the Expected Credit Loss (ECL) framework. The framework applies to scheduled commercial banks, including foreign banks, and introduces a risk-sensitive approach to provisioning. These are expected to further support credit risk management practices, promote greater comparability across financial institutions, and align regulatory norms with globally accepted regulatory and accounting standards.

7. Proactive stress management: The RBI’s Prudential Framework for Resolution of Stressed Assets promotes early identification, reporting, and time-bound resolution of stressed loans, with incentives for lenders to act swiftly.

Evolving Priorities in India’s Banking Landscape

| Priority Area |

Objective |

Key Actions |

Expected Impact |

| Strengthen Deposit Mobilization |

Sustain credit growth and liquidity |

Targeted deposit drives; optimized branch networks; outreach in semi-urban and rural areas |

Ensures adequate funds for lending and strengthens financial stability |

| Identify Emerging Growth Areas |

Enhance profitability and maintain economic momentum |

Focus on high-growth sectors over the next decade |

Positions banks for long-term sustainable growth |

| Deepen Corporate Lending |

Support productive sectors while managing risk |

Expand lending to key industries; robust underwriting and risk management |

Balances profitability with financial prudence |

| Advance Green Growth Agenda |

Promote sustainable energy and innovation |

Scale up lending to renewable energy; develop credit models for SMRs |

Supports India’s net-zero goals; banks become partners in green growth |

| Broaden Financial Inclusion |

Expand banking access to underserved populations |

Leverage schemes like PM MUDRA Yojana, PM Vishwakarma, PM Surya Ghar Muft Bijli Yojana, PM Vidyalaxmi, KCC |

Promotes inclusive growth and reduces financial inequality |

| Strengthen Agri Credit |

Boost farm productivity and rural economic growth |

PM Dhan Dhanya Yojana in 100 low-productivity districts; customized credit products |

Enhances rural livelihoods and local economic development |

| Expand International Presence |

Support India’s global financial integration |

Strengthen operations in GIFT City; participate in IIBX |

Positions India as a global financial hub |

| Enhance Customer Experience |

Improve accessibility and satisfaction |

Faster grievance redressal; multilingual digital platforms; modern physical branches |

Increases adoption, trust, and engagement with banking services |

Conclusion

India’s banking sector has transformed from a period of stress to one of strength and stability. With cleaner balance sheets, robust capital buffers, and record profitability, banks today are more resilient, efficient, and future-ready. Driven by reforms, digital innovation, and financial inclusion, the sector is powering India’s growth ambitions- financing infrastructure, supporting entrepreneurs, and advancing green and inclusive development. As India moves toward becoming the world’s third-largest economy, its banks stand at the forefront- anchoring financial stability and fuelling the nation’s next decade of growth.

Best ias coaching in delhi Best economics services coaching

No Comments