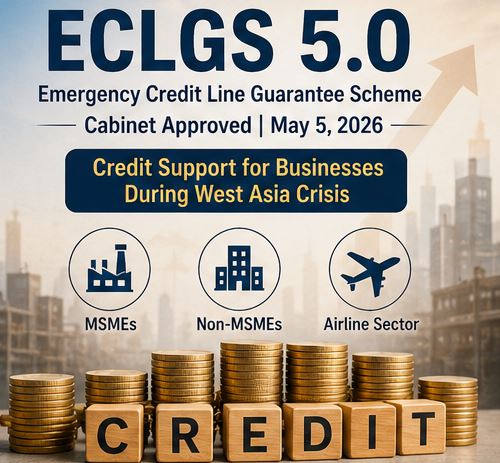

06 May Emergency Credit Line Guarantee Scheme 5.0

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 3 : Economy

FOR PRELIMS : Features of ECLS, Sectors it covers, etc.

FOR MAINS : The West Asia conflict has exposed deep structural vulnerabilities in India’s economy, particularly its dependence on external energy supplies and the fragility of its MSME sector. Analyse the economic impact of the West Asia crisis on India and evaluate the adequacy of the government’s policy response, including ECLGS 5.0.

Why in News?

On May 5, 2026, the Union Cabinet chaired by Prime Minister Narendra Modi approved the Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 — a targeted credit guarantee intervention designed to protect Indian businesses, especially MSMEs and the airline sector, from the liquidity stress caused by the ongoing West Asia conflict. The scheme aims to catalyse a total additional credit flow of ₹2,55,000 crore (including ₹5,000 crore dedicated to airlines) through a 100% guarantee for MSMEs and 90% guarantee for non-MSMEs and the aviation sector, administered by the National Credit Guarantee Trustee Company Limited (NCGTC).

Background: Understanding the West Asia Crisis and Its Impact on India

The Geopolitical Context

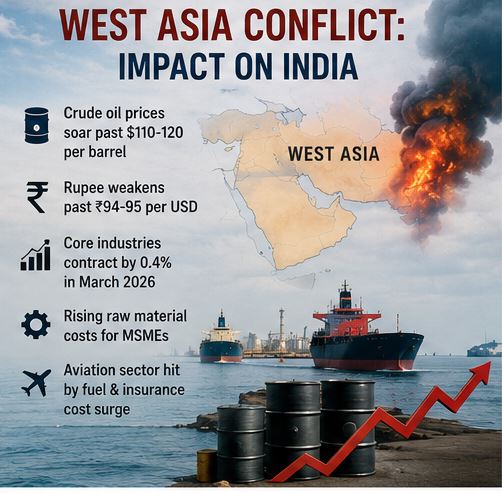

- The West Asia conflict (beginning around February–March 2026) has rapidly escalated into one of India’s most severe external economic shocks in recent decades.

- Critical trade arteries — particularly the Strait of Hormuz — have been severely disrupted, affecting global flows of crude oil, natural gas, fertilisers, and goods.

- India imports close to 90% of its crude oil and 50% of its natural gas from West Asian nations, making it acutely exposed to this crisis.

Economic Shockwaves on India

- Crude oil prices surged from approximately $62 per barrel before the conflict to over $110–$120 per barrel by mid-2026 — nearly double pre-war levels — creating severe inflationary pressures.

- The Indian Rupee has weakened past the ₹94–95 per USD mark, driven by elevated import costs and capital flight. Foreign Portfolio Investors withdrew nearly ₹1.8 lakh crore in 2026 — the steepest outflow on record.

- India’s eight core industries contracted by 0.4% in March 2026 — the first contraction in several quarters — against a growth of 3.5% in March 2025.

- Manufacturing sector PMI dipped to 53.8 in March 2026, reflecting rising costs and widespread uncertainty.

- Raw material costs for MSMEs surged: packaging materials (polymers, PET resin, HDPE) rose 30–60%, and petrochemical inputs like polypropylene and PVC saw steep price escalations.

- The aviation sector faced skyrocketing fuel costs, reduced route options, and surging insurance premiums.

- For the MSME sector specifically, the crisis triggered a classic “cost-price squeeze” — raw material costs escalated sharply while demand remained subdued, rapidly eroding working capital buffers.

Government Response Trajectory

- PM Modi convened a high-level Cabinet Committee on Security (CCS) meeting to assess implications for agriculture, aviation, shipping, logistics, and MSMEs.

- RBI extended export credit timelines, eased liquidity conditions, and deployed forex reserves to stabilise the rupee.

- The government announced a customs duty exemption on key petrochemical inputs (polypropylene, polycarbonate, PVC) until June 30, 2026.

- ECLGS 5.0 represents the most significant fiscal intervention in this response package.

What is the Emergency Credit Line Guarantee Scheme (ECLGS)? — Concept and Purpose

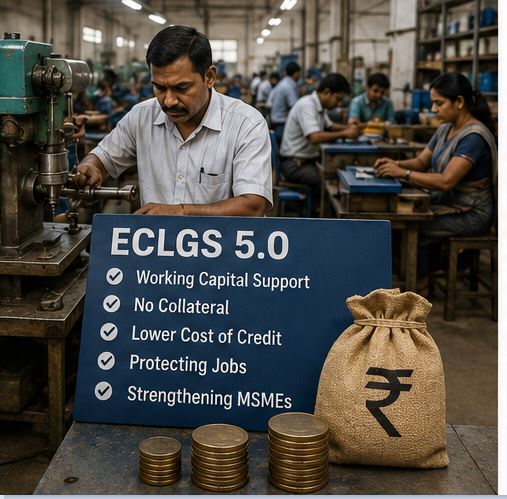

- ECLGS is a credit guarantee mechanism under which the government, through NCGTC (National Credit Guarantee Trustee Company Limited), provides guarantees to Member Lending Institutions (MLIs) — banks, Non-Banking Financial Companies (NBFCs), and Financial Institutions — against losses from loans extended to eligible borrowers.

- The core idea: Since MLIs bear the risk of default, they are often reluctant to lend to stressed borrowers. A government-backed guarantee eliminates or reduces this risk, incentivising banks to lend even in uncertain environments.

- Borrowers get additional working capital credit without the need for additional collateral, at reasonable interest rates, enabling them to survive short-term liquidity crunches without closing down or laying off workers.

Historical Evolution of ECLGS

The ECLGS framework has been India’s go-to counter-crisis credit instrument, deployed twice now in response to major economic shocks:

| Version | Year | Trigger | Key Target | Guarantee Cover | Credit Target |

|---|---|---|---|---|---|

| ECLGS 1.0 | May 2020 | COVID-19 Pandemic | MSMEs (outstanding ≤ ₹50 cr) | 100% | Part of ₹3 lakh cr |

| ECLGS 2.0 | Nov 2020 | COVID-19 (Sectoral Stress) | 26 Kamath Committee sectors + Healthcare (₹50–500 cr outstanding) | 100% | Part of ₹3 lakh cr |

| ECLGS 3.0 | March 2021 | COVID-19 (Hospitality/Tourism) | Hospitality, Travel, Aviation, Leisure sectors | 100% | Part of ₹3 lakh cr |

| ECLGS 4.0 | May 2021 | COVID-19 (Healthcare Oxygen Crisis) | Hospitals/Medical Colleges (oxygen plants) | 100% (up to ₹2 cr) | Extended ₹3 lakh cr |

| ECLGS 5.0 | May 2026 | West Asia Conflict | MSMEs, Non-MSMEs, Airlines | 100% (MSMEs) / 90% (others) | ₹2,55,000 crore |

ECLGS 1.0 (May 2020)

- Launched as part of the Aatmanirbhar Bharat Abhiyan — India’s COVID-19 economic relief package.

- Targeted MSMEs and business enterprises with total outstanding credit of up to ₹50 crore (with dues ≤ 60 days as on February 29, 2020).

- Additional credit: 20% of outstanding.

- Tenor: 4 years with a 1-year moratorium on principal.

- Guarantee: 100% coverage to MLIs.

ECLGS 2.0 (November 2020)

- Extended to businesses in the 26 COVID-stressed sectors identified by the Kamath Committee and the healthcare sector.

- Targeted borrowers with outstanding credit between ₹50 crore and ₹500 crore.

- Additional credit: 20% of outstanding.

- Tenor: 5 years with a 1-year moratorium.

ECLGS 3.0 (March 2021)

- Specifically targeted the hospitality, travel, tourism, leisure, sports, civil aviation, and floriculture sectors — the hardest-hit by COVID-19 travel restrictions.

- Enhanced additional credit to 40% of outstanding credit (up to ₹500 crore).

- Tenor: 6 years with a 2-year moratorium — the longest among all versions.

ECLGS 4.0 (May 2021)

- Launched during the second wave of COVID-19 to specifically address the oxygen crisis.

- Provided 100% guarantee for loans up to ₹2 crore to hospitals, nursing homes, medical colleges for setting up Pressure Swing Adsorption (PSA) oxygen plants.

- Also extended/revised earlier versions to accommodate restructured borrowers.

Outcomes of Earlier ECLGS Versions

- ECLGS (1.0–4.0 combined) enabled over 1.15 crore borrowers to access emergency credit.

- By FY2023, over ₹3.6 lakh crore was sanctioned and over ₹2.9 lakh crore disbursed.

- More than 85% of beneficiaries were micro and small businesses.

- The World Bank praised ECLGS as a case of “well-targeted government credit guarantee.”

- The scheme helped prevent mass layoffs and closures across labour-intensive sectors.

ECLGS 5.0 — Detailed Features and Structure

Administering Body : NCGTC (National Credit Guarantee Trustee Company Limited) — a Ministry of Finance entity — provides the guarantee cover to MLIs.

Eligible Borrowers

-

-

- MSMEs and Non-MSMEs (with existing working capital limits) whose accounts were standard as of March 31, 2026.

- Scheduled Passenger Airlines with outstanding credit facilities as of March 31, 2026, provided accounts are standard.

- Only borrowers with performing accounts (no NPA status) are eligible — this ensures the scheme supports viable businesses facing temporary stress, not structurally insolvent ones.

-

Guarantee Coverage

-

-

- 100% for MSMEs — full protection to lenders, maximising incentive to lend.

- 90% for Non-MSMEs and the Airline sector — MLIs bear 10% risk to retain lending discipline.

-

Guarantee Fee : Nil — no guarantee fee charged to borrowers or MLIs, reducing the cost of credit.

Quantum of Additional Credit

- MSMEs and Non-MSMEs: Additional credit of up to 20% of peak working capital utilised during Q4 FY2026 (October–March 2025-26), capped at ₹100 crore per borrower.

- Airline Sector: Additional credit up to 100% of peak working capital, capped at ₹1,500 crore per borrower, subject to specific conditions.

- Airlines receive a higher quantum and proportionately larger cap given their capital intensity and the severity of their exposure to fuel price shocks and disrupted air corridors.

Loan Tenor and Moratorium

| Category | Total Tenor | Moratorium |

|---|---|---|

| MSMEs and Non-MSMEs | 5 years from first disbursement | 1 year |

| Airline Sector | 7 years from first disbursement | 2 years |

Why is This Significant? — Multi-Dimensional Impact

Liquidity Bridge for MSMEs

- MSMEs — the backbone of India’s economy contributing over 30% of GDP and employing over 11 crore people — are the most vulnerable to working capital crunches during external shocks.

- Unlike large corporates, MSMEs lack access to bond markets, have limited cash reserves, and face acute difficulty in obtaining fresh credit during periods of uncertainty.

- ECLGS 5.0’s zero guarantee fee + 100% coverage for MSMEs is a direct signal from the government that the banking system should treat MSME credit as protected lending.

Aviation Sector — A Geopolitical Victim

- The West Asia conflict has dramatically impacted airlines through: surging aviation turbine fuel (ATF) prices, closure/rerouting of air corridors over conflict zones, rising insurance premiums, and reduced passenger demand.

- The ₹1,500 crore cap per airline borrower with a 2-year moratorium and 7-year repayment window is calibrated for the long recovery arc typical of the capital-intensive aviation sector.

- Preventing airline collapses also protects air connectivity, employment of pilots and ground staff, and the broader tourism ecosystem.

Employment Protection : Industries facing liquidity crunches typically resort to retrenchment as their first cost-cutting measure. By ensuring businesses can meet payroll, the scheme protects millions of jobs across the MSME and aviation supply chains.

Supply Chain Preservation : Many large manufacturers depend on a network of MSME suppliers and vendors. If these MSMEs collapse due to working capital stress, the entire supply chain is disrupted — damaging both domestic production and India’s export competitiveness.

Preventing Systemic NPA Risk

- Without liquidity support, even fundamentally viable MSMEs may default, converting temporary cash flow stress into permanent NPAs (Non-Performing Assets), damaging bank balance sheets and reducing future credit availability.

- ECLGS 5.0 acts as a pre-emptive shield against a potential wave of MSME NPAs.

Macroeconomic Stabilisation : By maintaining business operations, protecting supply chains, and preventing job losses, ECLGS 5.0 plays a counter-cyclical fiscal role — absorbing the shock before it translates into a broader demand collapse and economic contraction.

Key Institutional Mechanisms Involved

NCGTC (National Credit Guarantee Trustee Company Limited)

- Incorporated under the Companies Act as a Government of India company under the Ministry of Finance.

- Functions as the central guarantee manager for multiple government credit guarantee schemes.

- Issues the guarantee cover to MLIs, maintains the guarantee corpus, and processes claims.

Member Lending Institutions (MLIs) : Includes Scheduled Commercial Banks, NBFCs, Regional Rural Banks (RRBs), and Financial Institutions registered with NCGTC to participate in the scheme.

Expenditure : The guarantee corpus and scheme expenditure are backed by the Government of India’s fiscal commitment — this is effectively a contingent liability on the Union Budget, similar to previous ECLGS versions.

Challenges and Concerns

Implementation Speed vs. Crisis Timeline : The West Asia conflict is a time-sensitive crisis. The real-world benefit of ECLGS depends on how quickly banks process and disburse loans. Past experience shows bank-level KYC, credit assessment, and documentation requirements can slow disbursements considerably.

Structural vs. Temporary Stress : ECLGS only addresses liquidity stress (short-term cash flow gaps), not solvency stress (structural unviability). Businesses that were already struggling before the conflict may use the credit window without any genuine recovery path, eventually adding to NPAs.

Awareness Gap — Especially for Micro Enterprises : As seen in previous ECLGS rounds, micro-enterprises in rural and semi-urban areas often lack awareness of government schemes or face difficulties in meeting bank documentation requirements, limiting their actual access.

Conflict Duration Uncertainty : The scheme is calibrated on the assumption that the West Asia conflict will be relatively short-lived. A prolonged conflict beyond March 2027 may require further extensions or a more structurally redesigned intervention.

Airline Sector Structural Issues : India’s aviation sector has long suffered from structural weaknesses — high ATF taxes, aggressive pricing, thin margins. ECLGS credit provides liquidity but cannot fix these underlying structural deficiencies.

Prelims Question

Q. With reference to the Emergency Credit Line Guarantee Scheme (ECLGS) 5.0, recently approved by the Union Cabinet, consider the following statements:

- The scheme provides 100% credit guarantee coverage to both MSMEs and the airline sector.

- The guarantee under ECLGS 5.0 is administered by the National Credit Guarantee Trustee Company Limited (NCGTC).

- The additional credit for airlines under ECLGS 5.0 is capped at ₹1,500 crore per borrower with a moratorium of 2 years.

- ECLGS was first launched as part of the Aatmanirbhar Bharat Abhiyan in response to the COVID-19 pandemic.

Which of the statements given above are correct?

(a) 1, 2 and 4 only

(b) 2, 3 and 4 only

(c) 1, 3 and 4 only

(d) 1, 2, 3 and 4

Correct Answer: (b) 2, 3 and 4 only

Explanation:

- Statement 1 is INCORRECT. ECLGS 5.0 provides 100% guarantee for MSMEs but only 90% guarantee for non-MSMEs and the airline sector. The airline sector does NOT receive 100% coverage — it receives 90%.

- Statement 2 is CORRECT. The guarantee cover under ECLGS 5.0 is indeed provided through NCGTC (National Credit Guarantee Trustee Company Limited), which is a Ministry of Finance entity.

- Statement 3 is CORRECT. Airlines are eligible for additional credit up to 100% of peak working capital, capped at ₹1,500 crore per borrower with a moratorium of 2 years and a total tenor of 7 years.

- Statement 4 is CORRECT. ECLGS was first launched in May 2020 as part of the Aatmanirbhar Bharat Abhiyan economic relief package in response to the COVID-19 pandemic-induced liquidity crisis.

Mains Questions

“The Emergency Credit Line Guarantee Scheme (ECLGS) has emerged as India’s primary counter-crisis credit instrument, first deployed during COVID-19 and now in response to the West Asia conflict.” Critically examine the design, evolution, and effectiveness of ECLGS, and analyse whether credit guarantee schemes are a sufficient response to recurring external economic shocks.

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments