15 May WPI More Than Doubles to 8.3% in April — Highest in 3.5 Years

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 3 : Economy

FOR PRELIMS : WPI , Inflation , Growth

FOR MAINS : “India’s inflation data for April 2026 confirms what economists have long warned: in a heavily import-dependent energy economy, a geopolitical shock in West Asia is not an external event — it becomes an Indian macroeconomic event within weeks.” Critically examine how the West Asia crisis has transmitted to India’s wholesale price level, and the structural reforms needed to reduce India’s vulnerability to energy-driven inflation shocks. (15 M)

Why in News?

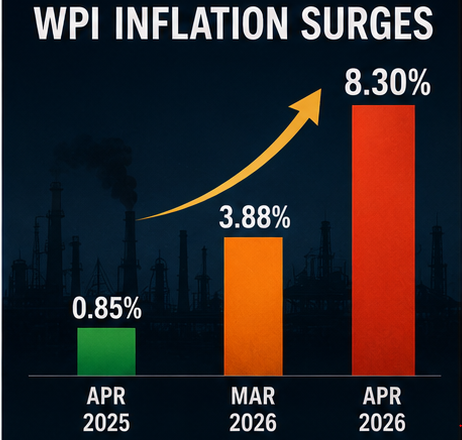

Data on the Wholesale Price Index (WPI) released by the Ministry of Commerce and Industry (DPIIT) on Thursday, May 14, 2026 showed India’s wholesale inflation jumped to 8.3% in April 2026 — from 3.88% in March and just 0.85% in April 2025 — its highest level in 3.5 years (since October 2022). The surge was driven overwhelmingly by the West Asia crisis and the Strait of Hormuz blockade, which pushed global crude oil prices above $120 per barrel, sending fuel and power inflation to 24.71% in April — up from a mere 1.05% in March. Crude petroleum inflation hit a staggering 88.06% year-on-year in April — meaning wholesale crude prices were nearly double those of a year ago. Experts from Bank of Baroda, Bajaj Broking, and India Ratings warned that wholesale inflation at this level will inevitably pass through to consumer prices and erode corporate profit margins — unless the government raises retail fuel prices, which OMCs are already losing ₹1,000 crore per day selling below cost. The overall WPI index rose from 160.8 to 167, a month-on-month jump of 3.86% — the sharpest single-month spike in at least six months.

What is WPI? — Understanding the Index

The Wholesale Price Index — Definition and Scope

The Wholesale Price Index (WPI) measures the average change in prices of goods at the wholesale or producer stage — before they reach the final consumer. It tracks price changes from the seller’s perspective in the first major transaction in the production chain, not the retail buyer’s perspective. In India, WPI is compiled and released by the Department for Promotion of Industry and Internal Trade (DPIIT) under the Ministry of Commerce and Industry, on a monthly basis, approximately two weeks after the reference month ends.

Base year: 2011-12 = 100 (revised from 2004-05 in 2017)

Number of items: 697 commodities tracked

Three major groups: (1) Primary Articles — 22.62% weight; (2) Fuel & Power — 13.15% weight; (3) Manufactured Products — 64.23% weight

Frequency: Monthly; provisional data released ~14 days after month end; revised twice

WPI: Measures wholesale/producer prices; no services included; higher weight for fuels; reflects input cost pressures; released by DPIIT

CPI: Measures retail/consumer prices; includes services (housing, education, health); lower fuel weight; reflects what households actually pay; released by MoSPI; used by RBI for monetary policy targeting (4% ±2% band)

WPI Category Weights — Why Fuel Dominates the April Reading

The Base Effect — Why April Numbers Are Extra Alarming

One important analytical dimension of the April 2026 WPI reading is the base effect. In April 2025 — before the West Asia war began — WPI inflation was a low 0.85%. This very low base means that even a moderate rise in wholesale prices in April 2026 would show up as a large percentage increase. However, experts caution that in this case, the rise is not merely a statistical artefact — the month-on-month jump of 3.86% (from index 160.8 in March to 167 in April) is independently alarming, confirming that actual price pressures are real and compounding, not just a base-effect illusion.

- Definition: Base effect refers to the impact of the comparison year (base) on the percentage change calculation. A very low base (April 2025 WPI = 0.85%) amplifies the year-on-year percentage change in April 2026

- Example: If wholesale prices were 100 in April 2025 and rose to 108.3 in April 2026, that’s an 8.3% increase. If the April 2025 base had been higher (say, prices were elevated then), the same April 2026 level would show a smaller % change

- April 2026 situation: The sector witnessed deflation of 7.6% and 15.5% in March and April 2025 — meaning fuel prices were already depressed in the base year, making April 2026’s 24.71% fuel inflation even larger than it would have been with a normal base. The base effect is thus amplifying — but not manufacturing — the April 2026 alarm signal

- Policy implication: Analysts expect the base effect to gradually fade from July 2026 onwards as the comparison period includes months post the start of the Iran conflict (February 2026) — which had already elevated prices. But the underlying crude shock must resolve for WPI to normalise

The WPI–CPI Divergence — A Tale of Two Indices

One of the most significant — and policy-consequential — features of April 2026’s data is the wide divergence between WPI (8.3%) and CPI (3.48%). India’s retail inflation (CPI) remains relatively moderate at 3.48% — within the RBI’s 2–6% comfort band — while wholesale inflation is running at more than twice that rate. This divergence is not sustainable, and experts warn it represents a stored-up inflationary pressure that will eventually arrive at consumers’ doorsteps.

1. Government price controls: Retail petrol, diesel, and LPG prices have been frozen — the government and OMCs are absorbing the crude surge. WPI picks up wholesale/refinery-gate prices; CPI picks up the frozen pump price. The divergence is the direct measure of the government’s artificial price suppression

2. Higher fuel weight in WPI: Fuel & Power has a 13.15% weight in WPI but only ~5.6% in CPI — magnifying the same crude shock in WPI relative to CPI

3. Transmission lag: Even uncontrolled prices take time to flow from wholesale to retail stages — typically 2–3 months

Scenario A — Fuel price hike: If the government raises petrol/diesel prices (as Puri hinted), CPI will jump sharply in that month — Bajaj Broking estimates a ₹10/litre diesel hike would add ~0.3–0.4 percentage points to CPI directly, and more through freight inflation

Scenario B — No hike: OMC losses continue at ₹1,000 crore/day; wholesale-to-retail pass-through happens through logistics and manufacturing cost raises anyway — CPI rises more slowly but rises inevitably. Corporate margins compress first; then prices rise.

Expert Views — What Analysts Are Warning

“This is a direct result of the global developments which have manifested on the oil front. The first sign of the impact of war on the Indian economy has been seen in the WPI inflation number for April, which came at 8.3%.”

“The rise in wholesale inflation was largely driven by higher crude oil prices, fuel and power costs, imported inflation, and elevated input prices amid the ongoing geopolitical tensions in West Asia. Higher logistics, freight, and commodity prices are now increasingly getting reflected in wholesale inflation, which could eventually pass through to consumer inflation.”

“The headline WPI inflation is likely to further rise to 9% in May 2026, due to transmission of high-energy prices and via its users, i.e. the manufacturing sector. WPI is expected to be higher than CPI on account of higher weight of fuels in the index, as well as the delayed transmission of high crude prices to consumers as the government and OMCs absorbed most of it until now.”

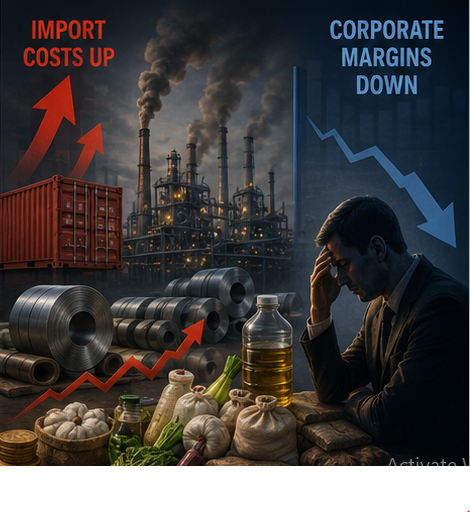

Margin Pressure on Companies — The Corporate Profitability Warning

The WPI surge carries a direct threat to corporate profit margins. When input costs (raw materials, energy, freight) rise at the wholesale level but companies cannot immediately pass them to customers, margins are squeezed. The April 2026 data shows this pressure building across multiple sectors:

| Sector | WPI input cost pressure | Margin risk | Pass-through ability |

|---|---|---|---|

| Logistics & transport | Diesel up 25.19% YoY | Very high — fuel is 30–40% of operating cost | Partial — freight rate hikes possible but lagged |

| Steel & basic metals | Basic metals inflation 7% | High — coking coal and energy cost pressure | Moderate — long-term contracts constrain flexibility |

| Textiles & garments | Textiles inflation 7.3%; cotton 22%+ | High — raw cotton and polyester costs elevated | Low — export orders at fixed price; domestic competition |

| Chemicals & fertilisers | Chemicals 5.09%; ammonia 20%+ | High — petrochemical inputs surge with crude | Moderate — fertiliser prices partly controlled by government |

| Aviation | ATF (Jet fuel) prices elevated | Very high — fuel is 35–45% of airline costs | Partial — higher fares possible; airlines cutting some international routes |

| Food processing | Edible oil up 22%; sugar cost elevated | Medium — commodity input pressure | High — FMCG companies have strong retail pricing power |

| IT / Software services | Minimal direct exposure to fuel/metal costs | Low — largely insulated | N/A — services not tracked in WPI |

RBI’s Dilemma — Inflation vs. Growth

The WPI surge places the Reserve Bank of India (RBI) in a delicate position. The RBI’s monetary policy framework targets Consumer Price Index (CPI) inflation at 4% (±2%) — not WPI. With CPI at 3.48%, still within the comfort band, the RBI has maintained its repo rate at 5.25%. However, a WPI-to-CPI pass-through is widely expected, and the RBI must decide whether to pre-emptively tighten or wait for the transmission to materialise.

- Rate hike (pre-emptive tightening):Would signal RBI’s resolve against future inflation; supports rupee by attracting capital inflows; but risks slowing already-stressed economy (UBS has downgraded FY27 GDP to 6.2%)

- Rate pause (current stance — “cautious”):Appropriate if CPI stays contained; allows growth to continue; but risks being behind the curve if WPI→CPI pass-through accelerates in May–July 2026

- Rate cut (unlikely in current environment):Would boost growth but would be pro-inflationary at a time when both WPI and the rupee are under pressure; would weaken rupee further

- CRR/SLR tools:RBI may use liquidity management tools (CRR, open market operations) to drain excess liquidity without formally changing the repo rate — a middle path

- Exchange rate management:A stronger rupee (via RBI forex intervention) would directly lower import costs and dampen WPI — but requires using India’s depleted forex reserves ($38 Bn fall in 2 months), creating a conflict with the forex conservation objective

Prelims Question

Q. With reference to the Wholesale Price Index (WPI) in India, consider the following statements:

1. The WPI in India is compiled and released by the Department for Promotion of Industry and Internal Trade (DPIIT) under the Ministry of Commerce and Industry, with base year 2011-12.

2. Manufactured Products carry the highest weight in India’s WPI at approximately 64.23%, followed by Primary Articles at 22.62% and Fuel & Power at 13.15%.

3. The Reserve Bank of India (RBI) uses WPI as its primary inflation target for monetary policy purposes, and is mandated to keep WPI-based inflation within a band of 4% ±2%.

4. A “base effect” in inflation measurement refers to the influence of the price level in the comparison (base) period on the percentage change calculation — a very low base period price level tends to inflate the percentage change in the current period.

Which of the statements given above are correct?

Statement 1 is CORRECT. India’s WPI data is compiled and published by the Office of the Economic Adviser (OEA) within DPIIT, under the Ministry of Commerce and Industry. The current series uses 2011-12 as the base year — revised from the earlier 2004-05 series in 2017. Data is released provisionally about 14 days after the reference month ends and is subsequently revised twice as more response data comes in.

Statement 2 is CORRECT. The weight distribution in India’s WPI (2011-12 series) is: Manufactured Products — 64.23% (highest weight; covers 555 of the 697 commodities); Primary Articles — 22.62% (food + non-food agricultural goods, minerals); Fuel & Power — 13.15% (coal, mineral oils, electricity). This weight distribution explains why Manufactured Products inflation, even at a moderate 4.62%, still contributes significantly to the headline WPI — while Fuel & Power at 13.15% weight but 24.71% inflation made the single largest percentage-point contribution to April 2026’s 8.3% reading.

Statement 3 is INCORRECT. The RBI does NOT target WPI for monetary policy. India’s Flexible Inflation Targeting (FIT) framework — enacted through the RBI Act amendment in 2016 — mandates the RBI to target Consumer Price Index (CPI) inflation at 4% with a tolerance band of ±2% (i.e., 2–6%). The RBI’s Monetary Policy Committee (MPC) sets the repo rate based on CPI data, not WPI. This is why in April 2026, despite WPI at 8.3%, the RBI held its repo rate at 5.25% — because CPI (3.48%) was well within the 4% ± 2% target band.

Statement 4 is CORRECT. The base effect is a standard concept in inflation analysis. When the base (comparison) period has very low prices, even a modest absolute rise in prices in the current period produces a large percentage increase. In April 2026, this is visible in the fuel sector — the base year (April 2025) saw fuel sector deflation of 7.6–15.5%, meaning fuel prices were depressed then. The same absolute level of fuel prices in April 2026 therefore produces a larger YoY percentage increase than it would if the base had been higher. The base effect is real but does not negate the underlying inflationary pressure in the current case, since the MoM jump of 3.86% is independently alarming.

Mains Questions

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments