15 May “Global Capital Comeback? India Weighs Tax Cut and Key Reforms”

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 3 : Economy

FOR PRELIMS : Investments , Growth , Taxation

FOR MAINS : “India’s foreign investment framework has long been characterised by two contradictory impulses — an eagerness to attract capital and a reluctance to fully liberalise the tax and regulatory environment needed to do so. The West Asia crisis of 2026 has forced this contradiction into the open.” Critically examine India’s capital account management challenges and evaluate the adequacy of the proposed policy measures. (15 M)

Why in News ?

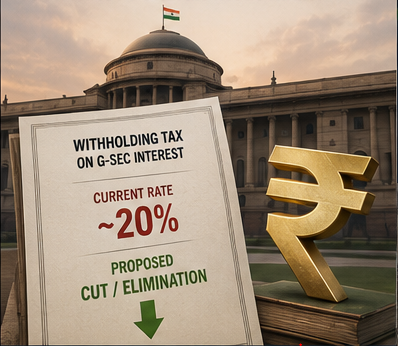

The Withholding Tax Problem — What It Is and Why It Matters

What Is Withholding Tax?

Withholding tax (also called Tax Deducted at Source for non-residents) is a tax deducted at source and paid by foreign investors on the interest income they receive on their holdings of Indian bonds. When a non-resident buys an Indian government security and receives interest, the issuer (the Indian government, through the RBI) deducts the withholding tax before remitting the interest to the foreign investor. The foreign investor thus receives the net-of-tax interest, which is taxed in India before it even leaves the country.

At present, non-residents pay withholding tax of approximately 20% on interest income on Indian government bonds — plus a surcharge, bringing the effective rate potentially higher. A concessional rate of 5% had been applied briefly (ending in 2023).

The 20% rate makes Indian bonds significantly less attractive compared to similarly-rated Emerging Market peers where withholding taxes are typically 0–10%.

A 20% withholding tax directly reduces the net yield received by the foreign investor. If India’s 10-year bond yields 7%, a 20% withholding tax reduces the effective post-tax yield to approximately 5.6%.

Compare this to US Treasuries at ~4.5% with zero withholding tax for most treaty-country investors — the after-tax yield difference is minimal, failing to compensate for India’s currency and geopolitical risk

Historical Evolution of Withholding Tax on Indian Bonds

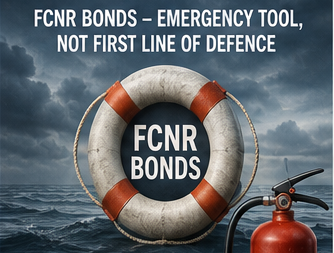

FCNR Bonds — The Emergency Capital Tool

Alongside the withholding tax discussion, policymakers are separately considering a fresh window for Foreign Currency Non-Resident (FCNR) bonds — a special instrument that allows India to raise foreign currency directly from the Indian diaspora (NRIs and PIOs) and other investors. FCNR bonds should remain in the toolkit as a fire extinguisher, not the first line of defence — because offering concessional windows to NRIs when US yields are 4–4.5% would mean a higher cost of capital for India and would effectively subsidise domestic savers.

| Feature | FCNR (B) Deposits | NRI Bonds / FCNR Sovereign Bonds |

|---|---|---|

| Currency | Foreign currency (USD, GBP, EUR, JPY, AUD, CAD) | Foreign currency; sovereign-guaranteed |

| Eligibility | NRIs and PIOs (Persons of Indian Origin) | NRIs, PIOs, and QFIs (Qualified Foreign Investors) |

| Interest | LIBOR-based + spread; regulated by RBI | Concessional rate set by government; swap facility available |

| Tenure | 1–5 years | Typically 3–5 years |

| Exchange rate risk | Borne by the Indian bank (hedged via RBI swap) | Borne by the government if swap offered |

| Precedent | 1998 Resurgent India Bonds ($4.2 Bn); 2000 India Millennium Deposits ($5.5 Bn); 2013 FCNR(B) scheme ($34 Bn raised) | Being discussed for 2026 under West Asia crisis conditions |

| Risk | Rollover risk when deposits mature; forex burden | Expensive if US yields remain elevated (4–4.5%) |

Three Things India Must Do to Win Back Foreign Investors

Beyond the immediate withholding tax fix, economists argue that India needs a sequenced, time-bound, big-bang reform package to restore foreign investor confidence. The three priorities, as articulated by Sachchidanand Shukla (Group Chief Economist, L&T) and echoed by other analysts, are:

The first priority is bold macroeconomic stabilisation signalling. Tax reform — specifically, evaluating a shift to a residence-based capital gains tax system that exempts foreign investors from long-term capital gains tax — would remove a major irritant that currently deters foreign portfolio investors. Long-term capital gains are currently taxed at 12.5% plus surcharge, and indexation benefits have been removed for property and gold. Exempting non-residents from Indian CGT would have universal impact and requires legislative action. Another measure would be to allow European UCITS funds to access India directly — giving them a passport into the market, though this could take longer.

Additionally, domestic fuel prices must be raised to reflect market realities — demand-side adjustments are necessary, followed by reform of inefficient subsidies, especially fertilisers. Without this, the fiscal deficit will widen and macro credibility will suffer.

The second priority is boosting India’s attractiveness as a destination for long-term foreign direct investment. FDI ownership caps could be revisited — including allowing 100% per cent automatic FDI in remaining sectors. India’s FDI story remains resilient: 90% of sectors are on the automatic route; investments from land-border countries (China-adjacent states) have been eased. Ownership below 10% is automatic, and electronics and polysilicon approvals are now within 60 days.

Even the PN3 (Press Note 3) rules could be refined by lowering the screening threshold and adopting a screening system similar to America’s CFIUS (Committee on Foreign Investment in the United States), to manage geopolitical exposure. Closing infrastructure gaps and delivering on budgeted capex would signal macro credibility. Labour reform — increasing workforce participation to 65%, with a push to labour-intensive sectors and agro-processing — would make exports more sustainable.

The third priority is the transformation of India’s economy for the long term. India must push decisively for trade liberalisation and integration into global value chains — including managing tariff tensions with ASEAN and the EU, alongside extending PLI incentives to labour-intensive sectors. Judicial reform is a grassroots pillar: AI-enabled case management and fast-track commercial courts could resolve disputes within months rather than years. A new version of the national single-window system would simplify approvals. Countries like Poland’s judicial efficiency reforms that unlocked economic dynamism offer a model.

Distribution reforms in the energy sector — specifically, electricity and petroleum products under GST — must also be acted upon. Financial deepening — a robust corporate bond market to pool domestic savings — would reduce volatility from foreign portfolio outflows by providing deeper domestic capital.

India’s FDI Story — Global Context and Competitiveness Gap

India’s broader foreign investment challenge goes beyond the immediate rupee crisis. According to UNCTAD, global FDI in 2025 stood at $1.6 trillion. While flows to developed economies rose 14% to $1.36 trillion, flows to developing economies fell 2% to $877 billion. India’s FDI fell 14 per cent to $50.5 billion in the same period.

| Dimension | Current Situation | Reform Proposed |

|---|---|---|

| Capital gains tax on FPI | 12.5% LTCG + surcharge; indexation removed; deters FPIs | Residence-based CGT system; exempt non-residents from LTCG on Indian securities |

| FDI sectoral caps | Most sectors on automatic route; a few restricted | 100% automatic FDI in remaining sectors; streamline approvals further |

| PN3 (Press Note 3) screening | All investments from land-border countries require government approval | Refine threshold; adopt CFIUS-style screening to manage geopolitical risk transparently |

| UCITS fund access | European UCITS funds cannot directly access India | Create a passport mechanism for UCITS — significantly expands the investor base |

| Infrastructure & capex | Gaps in cold chains, ports, roads; capex delivery sometimes delayed | Close infrastructure gaps; deliver budgeted capex on time to signal credibility |

| Labour laws | Labour reform pending; 4 codes passed but not all states notified | Finalise all four Labour Codes; increase workforce participation to 65%; PLI for labour-intensive sectors |

| Judicial efficiency | Average commercial dispute resolution: 3–5 years | AI-enabled case management; fast-track commercial courts; new single-window approval system |

| Energy sector distribution | Electricity and petroleum outside GST; state DISCOMS under financial stress | Bring electricity and petroleum under GST; financial deepening of energy sector |

The Capital Account and Currency — Why All of This Matters

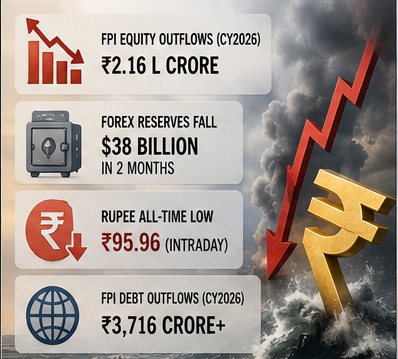

The Capital Account records all cross-border transactions involving financial assets — FDI, FPI equity, FPI debt, External Commercial Borrowings (ECBs), and NRI deposits. India’s capital account has come under severe stress in 2026:

- FPI equity outflows:₹2.16 lakh crore (CY2026) — foreign portfolio investors fleeing to safer markets; largest contributor to rupee pressure

- FPI debt outflows:₹3,476 crore from Debt (General Limit) + ₹240 crore from Debt (VRR) — even debt investments losing ground

- Forex reserves:Fell $38 billion in 2 months; total reserves ~$650 billion — still large, but depletion rate is alarming

- Rupee:Down 6% YTD (calendar year 2026); down 8%+ in last one month; at all-time low of ₹95.96 intraday

- Current Account Deficit (CAD):IMF projects $84 billion in 2026; crude oil and gold imports the two largest drivers

- India’s buffer:Reserves at ~$650 billion; debt-to-GDP ratios manageable; CAD at ~2% of GDP — below the 4.8% crisis of 2012-13; but pace of deterioration is the concern

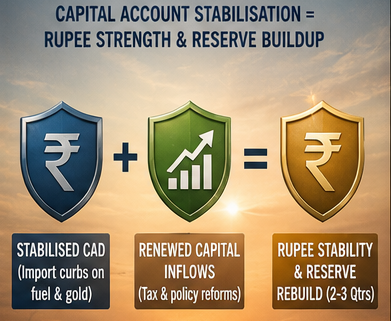

- The fix:A stabilised CAD (through fuel and gold import curbs) + renewed capital account inflows (through withholding tax cut, CGT reform, UCITS access) = rupee stabilisation + reserve rebuild over 2–3 quarters.

Prelims Question

1. Withholding tax on bond investments by non-residents in India is a tax deducted at source on the interest income received by foreign investors on their holdings of Indian bonds, and is governed by Sections 194LC and 194LD of the Income Tax Act.

2. India was included in JPMorgan’s Government Bond Index — Emerging Markets (GBI-EM) in June 2024, which brought significant passive index inflows into Indian government securities.

3. Foreign Currency Non-Resident (FCNR-B) deposits are available to all foreign investors including Foreign Portfolio Investors (FPIs) and Foreign Institutional Investors (FIIs), as long as they invest in Indian bonds.

4. The Capital Account in India’s Balance of Payments records cross-border transactions involving financial assets, including FDI, FPI equity and debt flows, External Commercial Borrowings (ECBs), and NRI deposits.

Which of the statements given above are correct?

Statement 1 is CORRECT. Withholding tax on non-resident bond interest in India is governed by Sections 194LC and 194LD of the Income Tax Act, 1961. Section 194LC covers interest on money borrowed in foreign currency from a source outside India (including government securities and long-term infrastructure bonds). Section 194LD covers interest on rupee-denominated bonds of Indian companies and government securities paid to FIIs and QFIs. Currently, the standard withholding rate on government security interest paid to non-residents is approximately 20%, with a concessional 5% rate that had been extended repeatedly until 2023 before lapsing. The proposed cut aims to restore or eliminate this withholding burden.

Statement 2 is CORRECT. India was formally included in JPMorgan’s Government Bond Index — Emerging Markets (GBI-EM) in June 2024, with a 10% weight cap — reflecting a long-standing recognition of India’s bond market’s depth and liquidity. This inclusion was expected to bring approximately $24 billion of passive index-tracking flows into Indian government securities, as global bond funds that track GBI-EM were required to purchase Indian G-secs to match the index weight. This was a landmark event for India’s bond market internationalisation.

Statement 3 is INCORRECT. FCNR(B) — Foreign Currency Non-Resident (Bank) — deposits are specifically designed for Non-Resident Indians (NRIs) and Persons of Indian Origin (PIOs). They are NOT available to all foreign investors including general FPIs or FIIs who are not of Indian origin. FCNR(B) is a diaspora-specific instrument where the NRI or PIO deposits foreign currency in an Indian bank for a fixed term (1–5 years) and receives interest — the exchange rate risk is borne by the Indian bank. General FPIs invest in Indian bonds through the Fully Accessible Route (FAR) or the Voluntary Retention Route (VRR), not through FCNR(B).

Statement 4 is CORRECT. India’s Balance of Payments has two main accounts: the Current Account (records trade in goods and services, remittances, investment income) and the Capital and Financial Account. The Capital and Financial Account records all cross-border transactions in financial assets — this includes FDI inflows and outflows, FPI equity and debt investments, External Commercial Borrowings (ECBs) raised by Indian companies abroad, NRI deposit inflows (including FCNR-B), and short-term capital flows. In 2026, India’s Capital Account has come under severe stress with ₹2.16 lakh crore in FPI equity outflows alone.

Mains Questions

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments