27 Jul Growth Theories

Growth Theories – UPSC Economics Optional Paper 1

Growth theories are central to understanding how economies expand their productive capacity and enhance living standards over time. As a key topic in Paper 1 of the UPSC CSE Economics Optional syllabus, students must master both the historical foundations and modern developments in growth theory to perform well in the exam.

📊 Infographic: Summary of Growth Theories

growth theories infographic

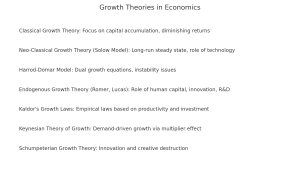

🧠 Mind Map: Growth Theories

growth theories mindmap

1. Classical Growth Theory

The classical school, led by economists like Adam Smith, David Ricardo, and Thomas Malthus, laid the foundation of growth economics in the late 18th and early 19th centuries.

Key Concepts:

- Law of Diminishing Returns: As population grows, output per worker diminishes due to limited resources.

- Stationary State: Economy reaches a point where growth halts due to resource constraints.

- Malthusian Trap: Population growth outpaces food supply, leading to famines and stagnation.

Classical theory emphasized supply-side constraints and pessimism regarding long-run growth unless external disruptions occurred (like wars or colonization).

2. Harrod-Domar Growth Model

This model, independently developed by Sir Roy Harrod and Evsey Domar in the 1930s and 40s, focuses on investment as the key driver of economic growth.

Best ias coaching in hindi medium

Best mentorship programme for upsc

Best ias coaching in chandigarh

Core Equations:

- Growth Rate (g) = s / v where s is the savings rate and v is the capital-output ratio.

- Emphasizes dual gap: savings gap and foreign exchange gap.

The model predicts either explosive growth or cumulative decline, due to the “knife-edge instability.”

Criticism:

- No role for technological progress.

- Unrealistic assumption of fixed coefficients.

- Fails to explain steady-state growth.

3. Neo-Classical Growth Theory (Solow Model)

Developed by Robert Solow (1956), this model introduced variable capital-labor substitution and exogenous technological progress.

Core Elements:

- Production Function: Y = F(K, L, A)

- Assumes diminishing marginal returns to capital and labor

- Steady state where growth is determined by population and technology

Golden Rule of Capital Accumulation:

Maximizes consumption per capita by choosing the optimal savings rate.

Criticism:

- Technological progress is exogenous and unexplained.

- Underestimates role of human capital and innovation.

GS paper 4 syllabus and study plan

GS paper 3 syllabus and study plan

4. Endogenous Growth Theory

Developed during the 1980s and 1990s by Paul Romer, Robert Lucas, and others to explain the source of technological progress within the model itself.

Features:

- Technology is a result of investment in human capital, innovation, and R&D.

- Increasing returns to scale and spillover effects.

- Growth is self-sustaining and policy-sensitive.

Important Models:

- Romer Model: Knowledge spillovers and increasing returns in production.

- Lucas Model: Emphasis on human capital accumulation.

- AK Model: Constant returns to capital; no diminishing returns.

5. Kaldor’s Growth Laws

Nicholas Kaldor proposed empirical laws based on UK data in the 1950s and 60s. He emphasized the role of the industrial sector in economic growth.

Kaldor’s Three Laws:

- GDP growth is positively related to the growth of the manufacturing sector.

- Productivity in manufacturing increases with output (Verdoorn Law).

- Faster growth of manufacturing leads to faster GDP growth.

These laws are empirical generalizations and have influenced development policy in several countries.

6. Keynesian Theory of Growth

While primarily focused on short-run aggregate demand management, Keynesian frameworks also contribute to growth theory.

Emphasis on:

- Effective demand as a driver of investment.

- Multiplier and accelerator effects.

- Underutilized resources as a basis for policy intervention to trigger growth.

Keynesian theory explains cyclical growth patterns and the role of fiscal policy in stabilizing output and employment.

7. Schumpeterian Growth Theory

Joseph Schumpeter emphasized the role of entrepreneurship, innovation, and creative destruction in economic progress.

best economics optional test series

best teacher of economics optional

Best economics optional coaching

Key Points:

- Innovation is the engine of capitalist growth.

- Old technologies and firms are replaced by new ones.

- Entrepreneurial risk-taking is essential for technological progress.

Modern Schumpeterian growth models like those by Aghion and Howitt build on this theory within an endogenous growth framework.

🔄 Comparative Summary of Growth Models

| Model | Capital Role | Technology | Policy Role |

|---|---|---|---|

| Classical | Central, diminishing returns | Absent | Minimal |

| Harrod-Domar | Fixed coefficients | Absent | Significant |

| Solow | Diminishing returns | Exogenous | Limited |

| Endogenous | Constant/increasing returns | Endogenous | Crucial |

| Kaldor | Sectoral focus (manufacturing) | Implied | Important |

| Keynesian | Multiplier-driven | Not primary | High |

| Schumpeterian | Through innovation | Endogenous | High |

📚 Previous Year UPSC Questions on Growth Theories

- Discuss the implications of the Harrod-Domar model for a developing economy like India. (2019)

- Compare and contrast the Solow and Endogenous Growth models. (2020)

- Critically examine Kaldor’s Growth Laws. (2022)

🔮 Probable Questions for UPSC Mains and Prelims

- How does Endogenous Growth Theory improve upon the Solow Model?

- Explain the role of innovation in Schumpeterian growth models.

- Compare Classical and Keynesian views on economic growth.

- Which growth model best explains India’s post-1991 growth trajectory?

No Comments