01 May Revenue Deficits: Reform, Responsibility, and Resilience

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 2, 3 (Government Policies & Interventions, Economy )

FOR PRELIMS : Fiscal Policy of India , Committees, Trends year wise.

FOR MAINS : Distinguish between ‘Fiscal Deficit’ and ‘Revenue Deficit’ in the context of Indian states. Why is the latter considered a more serious structural flaw in a state’s financial health? Suggest two measures to bridge the widening revenue gap.

Why in News?

The Union Finance Ministry’s Monthly Economic Review for April 2026 sounded a clear alarm: nine of the eighteen large States analysed by the Ministry are in revenue deficit as per their own projections for 2026–27. The Ministry warned that these states, burdened by high debt and recurring revenue shortfalls, will find it significantly harder to cope with fiscal shocks — including those emanating from the West Asia crisis — and may be forced to either reprioritise expenditure away from productive areas or approach the Centre for more funds, even as the Centre is itself trying to consolidate its own finances.

CONCEPTUAL FOUNDATION: UNDERSTANDING THE DEFICIT TAXONOMY

Revenue Deficit is the shortfall when a government’s revenue expenditure (salaries, pensions, subsidies, interest payments on existing debt) exceeds its revenue receipts (taxes, non-tax revenues). It signifies that the government is borrowing not to create assets but merely to meet its day-to-day running costs — a condition described in public finance as violating the Golden Rule of Public Finance.

Fiscal Deficit is the broader measure: the difference between total expenditure (revenue + capital) and total receipts excluding borrowings. It represents the government’s total borrowing requirement in a given year.

Primary Deficit equals fiscal deficit minus interest payments. It shows the current government’s fresh borrowing, distinct from the servicing of accumulated past debt.

Effective Revenue Deficit (ERD) = Revenue Deficit minus grants given for capital asset creation. This metric, introduced by India, distinguishes between truly wasteful borrowing and borrowing that at least flows into state-level capital formation.

CONSTITUTIONAL ARCHITECTURE OF FISCAL GOVERNANCE

Article 292 governs borrowing by the Union Government, empowering it to raise loans on the security of the Consolidated Fund of India, subject to parliamentary approval. The Comptroller and Auditor General (CAG) monitors and audits the use of borrowed funds to ensure compliance with constitutional and financial norms.

Article 293 is the most critical constitutional provision governing state-level fiscal discipline. Article 293 of the Indian Constitution provides that States have the authority to borrow money within India, secured by their Consolidated Fund, within limits set by their respective legislatures. However, they cannot borrow without the consent of the Government of India if any previous loans or guarantees from the Government of India are outstanding.

This provision has become a major constitutional battleground. The State of Kerala contests the validity of specific provisions of the FRBM Act, and of a letter from the Union imposing a Net Borrowing Ceiling (NBC) on the State, capping it at 3% of the projected Gross State Domestic Product (GSDP). Kerala argues that these measures violate Article 293 of the Constitution, asserting that the Union lacks authority to regulate all forms of state borrowings.

As Article 293 has never been substantially dealt with by the Supreme Court, the Kerala case has been referred to a five-judge bench. The Constitution does not intend to leave a State to its own devices completely in terms of fiscal management.

Articles 268–272 define the distribution of revenues between the Union and States. Article 275 provides for compulsory statutory grants-in-aid to States. Article 280 establishes the Finance Commission, constituted every fifth year, to recommend the distribution of taxes and grants between the Centre and States.

The Seventh Schedule delineates fiscal responsibilities — Public Debt of the State falls under the State List, giving states exclusive jurisdiction, yet the FRBM framework imposes central oversight, creating a structural tension in India’s cooperative federalism.

Article 266 creates the Consolidated Fund of India and the Consolidated Funds of States — the primary repositories of revenues, from which all expenditures (including debt servicing) must be authorised by Parliament or state legislatures respectively.

Finance Commission Recommendations

The 15th Finance Commission (2021–26) made specific recommendations on state borrowings: The Union government, as per the recommendations made by the FC-XV, allowed the State governments to borrow an additional 1% of their GSDP by relaxing the fiscal deficit target under the FRBM Act from 3.0% to 4.0% in 2021-22 and 3.5% in the subsequent year. Besides, an additional borrowing of 0.5% of GSDP was also allowed to the States for a four-year period from 2021-22 to 2024-25, made conditional and linked to power sector reforms at the State level.

The 16th Finance Commission (currently deliberating for the 2026–31 period) has already flagged the freebie problem. An analysis of 21 states by the Finance Commission showed that their subsidies and transfers were budgeted at ₹9.73 trillion in 2025-26, as against ₹3.86 trillion in 2018-19. As a percentage of the combined GSDP, the outlay on subsidies rose to 2.7 per cent in 2023-24 from 2.2 per cent in 2018-19.

RBI Guidelines

The Reserve Bank of India, as debt manager for states, issues annual reports on State Finances and issues guidelines on:

- Ways and Means Advances (WMA) limits — short-term liquidity support

- Overdraft regulations for states

- Market borrowing calendars and yield monitoring

- Off-budget borrowing surveillance

The RBI has consistently flagged that off-budget borrowings through State Public Sector Enterprises (SPSEs) and special purpose vehicles are understating the true fiscal stress of several states.

NITI Aayog’s Fiscal Health Index

In January 2025, NITI Aayog released the Fiscal Health Index (FHI) — a composite index evaluating states on five dimensions: expenditure quality, revenue mobilisation, fiscal prudence, debt index, and debt sustainability. This provides a granular, comparative picture of state-level fiscal health and is now an important reference tool for policy dialogues with state governments.

HISTORICAL TREND OF DEFICITS AMONG INDIAN STATES

The Pre-Reform Era (Pre-1991)

In the planned economy era, states were largely dependent on Central plan transfers and could run deficits with relative impunity, as the Centre would bail them out. Revenue deficits were endemic, not aberrations. The absence of hard budget constraints — a concept developed by economist János Kornai — meant states had little incentive for fiscal discipline.

Post-Liberalisation Fiscal Stress (1991–2003)

The 1991 balance-of-payments crisis forced fiscal consolidation at the Centre, but states lagged. The 1990s witnessed a deterioration of state finances: the combined revenue deficit of states widened dramatically, power sector losses ballooned (with state electricity boards accumulating losses), and pay commission implementations (particularly the Fifth Pay Commission in 1997) added enormous unfunded liabilities.

By the early 2000s, several large states — including Bihar, Uttar Pradesh, and West Bengal — were in a debt trap, spending more on interest payments than on development. The Twelfth Finance Commission (2005–10) recommended debt relief linked to fiscal reforms — a carrot-and-stick approach that produced measurable results.

Era of Fiscal Consolidation (2003–2008)

The enactment of the FRBM Act (2003) and its state equivalents produced remarkable results. Combined states’ revenue deficit turned into a surplus by 2007–08, reaching a record low by FY2008. This was aided by strong tax buoyancy from the high-growth period, improved GST compliance (state VAT at the time), and the debt-swap scheme that reduced interest burdens.

State Finances Revenue Deficit data reached a record low of −₹4,29,427 crore (surplus) in 2008. This represents the high watermark of state fiscal consolidation.

Post-Financial Crisis Deterioration (2008–2013)

The 2008–09 global financial crisis prompted a stimulus-driven expansion. Escape clauses were invoked, FRBM targets were suspended, and the Centre’s fiscal deficit rose above 6% of GDP. States followed suit. The stimulus, while necessary, was never fully withdrawn, and fiscal consolidation targets became moving goalposts.

Decade of Mixed Performance (2013–2020)

The introduction of the Goods and Services Tax (GST) in July 2017 was expected to improve state revenues. Instead, the transition brought unexpected headwinds. Since GST implementation in 2017, aggregate revenue from taxes subsumed under GST has declined from 6.5% of GDP in 2015-16 to 5.5% in 2023-24. The 15th Finance Commission had estimated a medium-term ratio of 7% revenue from GST. Most states collect lower revenue from GST than earlier.

The Fifth Pay Commission at the state level, loan waiver programmes (most prominently in Maharashtra and Uttar Pradesh in 2017–18), and rising pension liabilities began pressing state finances even in states that had previously been models of fiscal discipline.

Pandemic-Era Collapse and Recovery (2020–2022)

COVID-19 dealt the most severe blow. The combined states’ revenue deficit reached an all-time high of ₹37.12 lakh crore in 2021. Capital receipts collapsed, while expenditure on health and relief measures surged. The Centre relaxed borrowing norms but simultaneously centralised decision-making, leading to the Centre–State fiscal federalism tensions visible in the Kerala case today.

Post-Pandemic Stress Persistence (2022–2026)

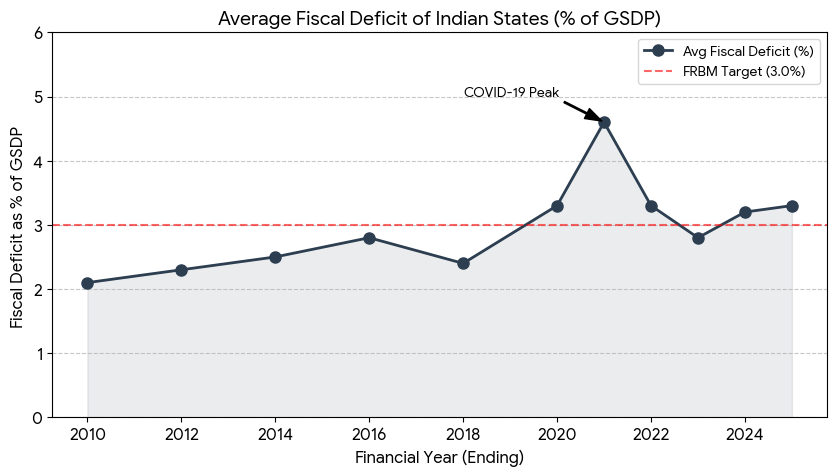

Despite a recovery in tax revenues, the combined gross fiscal deficit of States rose from 2.6% of GDP in FY22 to 3.2% in FY25, with outstanding liabilities at about 28.1% of GDP.

Fiscal deficit in 2024-25 was higher than that in 2005-06 in 15 states. Part of the reason for states exceeding the original fiscal deficit limit of 3% of GSDP is the relaxation by the Central government under specific circumstances such as power sector reforms, exclusion of long-term interest-free loans, and NPS contributions.

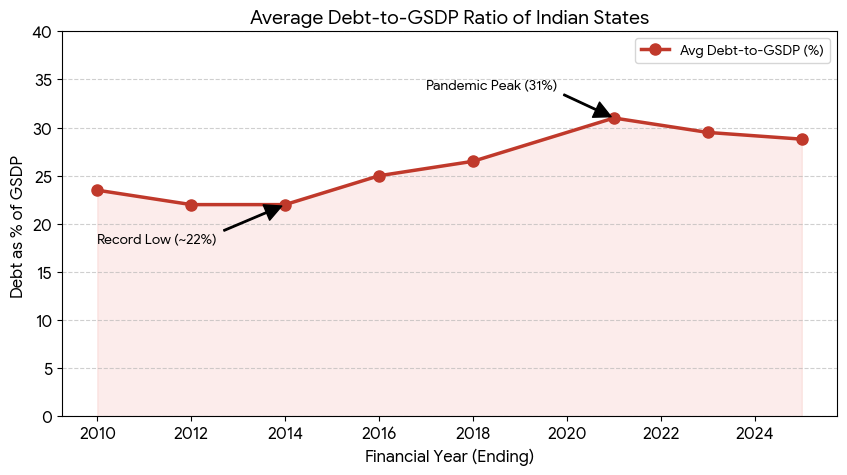

The aggregate outstanding debt of states now stands at 27.5% of GDP as of March 2025, leading to crowding out of expenditure on other development activities. Several states — particularly Punjab, Himachal Pradesh, Kerala, and Andhra Pradesh — have debt levels well above the FRBM-mandated 20% of GSDP.

THE COMPOUND CRISIS: WHY DEFICITS ARE WORSENING TODAY

Structural Weakness: Revenue Mobilisation Gap

India’s states suffer from a chronic inability to mobilise own-source revenues commensurate with their expenditure responsibilities. Property taxes remain grotesquely undervalued in most states. State excise, stamps and registration, and non-tax revenues have not kept pace with GDP growth. The GST’s centralization of revenue-raising, combined with a compensation mechanism that ended in 2022, has left states structurally dependent on Central devolution — devolution that is itself constrained by the Centre’s own fiscal pressures.

The Freebies Pandemic: Competitive Populism

This is the most immediately visible driver of revenue deficits today.

Many states are running a revenue deficit, which effectively means they are borrowing to fund subsidies or simply distributing cash under one scheme or another. Chief Justice of India Surya Kant noted that unchecked distribution of largesse could weaken the economic foundations of the country, and that announcements of such schemes frequently took place before elections.

According to the Economic Survey 2025–26, unconditional cash transfers and populist freebie schemes implemented across Indian States are estimated to cost approximately ₹1.7 lakh crore in FY26. Unconditional cash transfers account for a 20 per cent share in schemes for subsidies and transfers of states, with the biggest component being power subsidy at 27 per cent.

The numbers are staggering in their trajectory: subsidies and transfers were budgeted at ₹9.73 trillion for 2025-26 across 21 states, up from ₹3.86 trillion in 2018-19. This is an increase of 152% in just seven years — far outpacing both GSDP growth and state revenue growth.

Once announced, universal freebies become politically irreversible. Any rollback is branded anti-people. Governments across party lines then compete to outbid one another. Over time, welfare is no longer calibrated policy; it becomes competitive populism.

The Supreme Court’s intervention in February 2026 (hearing related to Tamil Nadu Power Distribution Corporation) is significant: the Court labelled it a “culture of freebies” and a potential threat to India’s fiscal stability, noting these schemes are strategically timed to influence voters rather than address genuine socio-economic needs.

The legal precedent from S. Subramaniam Balaji v. Tamil Nadu (2013) had earlier held that freebies fall within legislative policy and are beyond judicial scrutiny. However, the evolving judicial view in 2025–26 is more cautionary, reflecting the scale of fiscal damage.

Interest Payment Trap

Revenue-deficit states face a particularly vicious cycle: they borrow to meet current expenditure → this adds to outstanding debt → debt servicing (interest payments) grows → interest payments consume a rising share of revenue receipts → even more borrowing is needed. The Ministry of Finance noted that these states “carry, on average, significantly higher outstanding liabilities than revenue-surplus States, and many of them spend more than 15% of their revenue receipts on interest payments.”

For Punjab, interest payments now consume nearly 23% of revenue receipts. For Himachal Pradesh and Kerala, the proportion is similarly alarming. This is the debt trap in its classical form.

The West Asia Geopolitical Shock

The ongoing Iran-Israel-West Asia conflict is transmitting fiscal stress through multiple channels:

- Energy price volatility: Global crude oil prices have risen sharply, increasing the subsidy burden on states providing free/subsidised LPG, cooking gas, and electricity (which is partially coal/gas-dependent). Geopolitical tensions in West Asia have unsettled energy markets, and the effects are visible in domestic price pressures, including the recent LPG stress.

- Remittance risk: States like Kerala, whose fiscal health is partly sustained by NRI remittances that boost consumer demand and GST collections, face exposure if West Asian economies slow down.

- Inflation and welfare demand: Import-driven inflation raises the cost of providing subsidies at fixed prices, widening the gap between market prices and subsidised rates, thereby escalating the subsidy bill.

- Crowding out of capital expenditure: As states struggle to meet revenue commitments, capital expenditure — the growth-multiplying spending on roads, schools, and hospitals — is the first casualty. This is the most damaging long-run consequence.

Pension and Pay Commission Liabilities

The transition from the Old Pension Scheme (OPS) to the National Pension System (NPS) was expected to reduce long-term liabilities. However, several states — including Rajasthan (under previous government), Chhattisgarh, Jharkhand, Punjab, and Himachal Pradesh — have either reverted to OPS or are under intense political pressure to do so. The short-term relief of lower NPS contributions is massively offset by the long-term unfunded liability this creates. The RBI has estimated that a full reversal to OPS across all states could add liabilities equivalent to 4.5% of GDP.

Off-Budget Borrowings: The Hidden Iceberg

A critical structural issue is that the officially reported fiscal deficit understates the true extent of state borrowings. States route debt through Special Purpose Vehicles, State Public Sector Enterprises (like DISCOMs and road corporations), and guarantees that do not appear in the budget. The RBI and CAG have repeatedly flagged this issue. When off-budget liabilities are included, the true fiscal stress of states like Punjab, Kerala, and Andhra Pradesh is significantly higher than headline numbers suggest.

GST Revenue Underperformance

Since GST implementation in 2017, aggregate revenue from taxes subsumed under GST has declined from 6.5% of GDP in 2015-16 to 5.5% in 2023-24. This means states have less own-source revenue to fund their expenditures, making them more vulnerable when Central transfers are delayed or reduced.

Reduced Untied Transfers

Between the 11th and 14th Finance Commission periods, the share of untied transfers to states increased from 44% of total transfers to 68%. However, this declined during the 15th Finance Commission period. Lower untied grants reduce state flexibility and force greater reliance on borrowings.

SOLUTIONS: A MULTI-LAYERED REFORM AGENDA

Strengthening the FRBM Framework

The Fiscal Responsibility and Budget Management (FRBM) Act should be strengthened. Subsidy schemes should have ‘sunset clauses’ for periodic review and evaluation. Improve tracking of off-budget borrowings and hidden subsidies through strengthened financial regulators.

The NK Singh Committee’s recommended Independent Fiscal Council remains unimplemented — this is perhaps the most important institutional gap. An independent body would prevent creative accounting, provide credible forecasts, and insulate fiscal targets from political cycles.

Rationalising Subsidies: The DBT Revolution

Direct benefit transfers, tighter targeting, and periodic price adjustments can contain costs without diluting support. In fertilisers, a shift towards nutrient-based pricing and incentives for balanced usage can reduce distortions over time. Rationalisation of Centrally Sponsored Schemes and elimination of duplication can yield savings.

India’s JAM Trinity (Jan Dhan–Aadhaar–Mobile) provides the technological infrastructure to shift from universal in-kind subsidies to targeted cash transfers. Utilise the JAM Trinity for Direct Benefit Transfers to reduce leakage and ensure aid reaches only the needy, avoiding universal, indiscriminate handouts.

Global models are instructive: Mexico’s Progresa and Brazil’s Bolsa Familia demonstrate that Conditional Cash Transfers (CCTs) — which link financial support to health check-ups, school attendance, and other positive behaviours — build human capital while targeting the genuinely needy, avoiding the dependency trap.

Distinguishing Welfare from Freebies

A critical conceptual distinction must be institutionalised in policy:

- Welfare (Merit Goods): Spending on education, health, nutrition, water, and sanitation that builds human capital, fulfills constitutional obligations under Articles 38 and 47 (Directive Principles), and has demonstrable long-run economic returns.

- Freebies (Non-Merit Goods): Unviable, universal handouts — free consumer electronics, free electricity to all (not just the poor), waiver of loans for all farmers regardless of income — given primarily for electoral gains, with no long-term developmental rationale.

Establish policy guidelines differentiating essential welfare from electoral freebies using objective criteria such as social utility, long-term human development impact, fiscal sustainability, targeting effectiveness, and outcome orientation.

Electoral Reforms: Accountability in Manifesto Promises

What is required is perhaps the most consequential political reform since the liberalisation era: a clear amendment to the Representation of the People Act to mandate transparent distinction between legitimate, policy-backed welfare and competitive freebies, and to require costing and funding disclosures for all electoral promises.

The Election Commission’s 2022 guidelines requiring political parties to explain funding mechanisms are a step forward but lack enforcement teeth. An amendment mandating independent costing of manifesto commitments — similar to the Parliamentary Budget Office in Canada or the independent Office for Budget Responsibility in the UK — would introduce accountability.

The One Nation One Election proposal also carries a fiscal dimension: synchronised electoral cycles would reduce the constant political incentive to announce fresh doles in response to impending state polls. It would create longer, uninterrupted governance windows focused on policy execution rather than poll positioning.

Enhancing Own-Source Revenue Mobilisation

States must systematically improve their revenue base:

- Property tax reform: India’s property tax-to-GDP ratio is among the lowest in the world at ~0.2%. Digitalisation of land records and GIS-based property mapping can dramatically expand the tax base.

- Land monetisation: States sitting on vast government land can monetise these assets through long-term leases, joint development, and transparent auctions.

- Tourism and green economy levies: States with natural assets — forests, coasts, mountains — can introduce environment levies and ecotourism fees.

- GST compliance improvement: Analytics-driven GST audits, e-invoicing mandates, and coordination with GSTN data can improve state GST collections.

Reforming the Power Sector: The Single Largest Fiscal Drain

The DISCOM (electricity distribution company) crisis is the single largest off-budget fiscal liability of states. Power subsidies alone accounted for 27% of state subsidy expenditure. The conditions-based additional borrowing facility (linked to power sector reforms under the 15th Finance Commission) was a positive step, but implementation has been patchy.

The RDSS (Revamped Distribution Sector Scheme) and UDAY Scheme have improved AT&C (aggregate technical and commercial) losses, but political commitments to free electricity continue to erode discoms’ financial health. A time-bound transition from universal free power to targeted free power (only for Below Poverty Line households) is essential.

Cooperative Federalism in Fiscal Management

The Centre must play a constructive enabling role:

- Debt Restructuring Facility: For states in genuine debt traps (like Punjab), a one-time debt restructuring — linked to binding fiscal reform commitments — can break the cycle without creating moral hazard.

- Transparent Net Borrowing Ceiling (NBC): The formula-based NBC mechanism must be made transparent, predictable, and non-discretionary to avoid the fiscal federalism tensions visible in the Kerala case.

- Intergovernmental Fiscal Compact: The 16th Finance Commission has an opportunity to recommend a formal, binding fiscal compact between the Centre and States — one that links higher grants-in-aid to measurable fiscal responsibility indicators, creating a system of fiscal accountability with fiscal autonomy.

Capex Protection: The Non-Negotiable

At the Centre level, the lesson is clear: public capital expenditure should be protected, given its role in sustaining medium-term growth. The composition of spending will matter as much as its aggregate level.

For states, the same principle applies with even greater force. The states that consistently outperform — Odisha, Gujarat — are those that have protected capital expenditure even during fiscal stress, understanding that today’s capex is tomorrow’s revenue (through better infrastructure, more productive labour, and higher tax base).

Long-Term: Building Fiscal Institutions

India needs to invest in building the institutional infrastructure for long-term fiscal responsibility:

- State-level Fiscal Councils: Independent bodies at the state level, analogous to the NK Singh Committee’s recommended national fiscal council, to provide unbiased fiscal assessments.

- Fiscal Stability Reporting: Annual reports at both state and national levels mapping fiscal risks, similar to Financial Stability Reports published by the RBI for the banking sector.

- Credit Rating System for States: As recommended by CII, a transparent credit rating system would impose market discipline on states, incentivising fiscal prudence.

- Outcome-Based Budgeting: Shifting from input tracking to outcome monitoring — spending ₹100 crore on education should be evaluated by learning outcomes, not just expenditure.

-

- A “Revenue Deficit” in a State’s budget implies that the State’s total expenditure (including capital outlay) exceeds its total non-debt receipts.

- Under the current fiscal roadmap, the 50-year interest-free loans provided by the Centre for capital investment are excluded from the calculation of the 3% GSDP fiscal deficit limit for states.

- A persistent revenue deficit restricts a state’s “fiscal space,” often leading to the practice of using borrowed funds to meet day-to-day administrative expenses rather than asset creation.

A) 1 and 2 only

B) 2 and 3 only

C) 3 only

D) 1, 2, and 3

Answer: B

Reasoning: Statement 1 is incorrect because Revenue Deficit only considers revenue expenditure vs revenue receipts; it excludes capital transactions. Statement 2 and 3 reflect the current policy shift and the economic impact of revenue stress mentioned in the news.

“The emergence of recurring revenue deficits in half of India’s large states threatens the ‘quality of expenditure’ at the sub-national level.” In light of the Finance Ministry’s 2026 report, analyze how revenue stress forces states to compromise on productive capital outlay. (150 words)

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments