14 May Govt Tightens Grip on Gold Imports, Duty Jumps to 15%

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 3 : Economy

FOR PRELIMS : Duty Structure , CAD , Liberalised Remittance Scheme

FOR MAINS : “The simultaneous pressure on India’s external sector from crude oil, gold, the Liberalised Remittance Scheme, and FII outflows in 2026 reveals that India’s Current Account Deficit is not a single-variable problem — it requires a multi-instrument, coordinated policy response.” Analyse the drivers of India’s 2026 external sector stress and evaluate the adequacy of the policy measures deployed so far. (15 M)

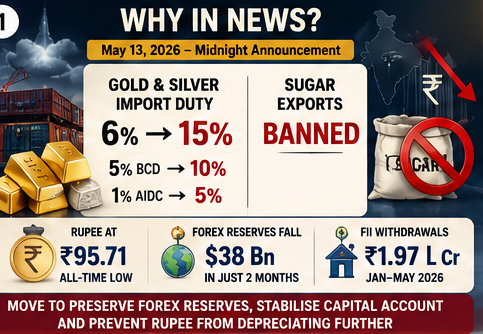

Why in News?

In a midnight announcement on Wednesday, May 13, 2026, the Union government hiked customs duty on gold and silver imports from 5% to 10%, and raised the Agriculture Infrastructure and Development Cess (AIDC) from 1% to 5% — taking the total effective import duty on precious metals to 15% from the earlier 6%. Simultaneously, the government banned sugar exports. These moves follow PM Narendra Modi’s 7-point austerity appeal, are designed to preserve India’s depleted foreign exchange reserves, and aim to bring stability to the capital account and prevent the rupee from depreciating further — which closed at ₹95.71 to a US dollar, having lost nearly 5% since the beginning of the West Asia conflict. India’s forex reserves fell by nearly $38 billion in just two months following the escalation of the conflict. As officials noted, “one quarter of losses can wipe out net profits made during the last financial year” — a description of how acute the strain has become.

The Duty Structure — Before and After

Before the midnight announcement, gold and silver imports attracted a total effective duty of 6% — comprising a 5% Basic Customs Duty (BCD) and a 1% Agriculture Infrastructure and Development Cess (AIDC). The government has now restructured both components sharply upward:

The BCD on gold and silver doubled — from 5% to 10%. This is the primary tariff component levied under the Customs Act, 1962, and goes directly to the Consolidated Fund of India. The doubling of BCD makes gold and silver physically 5 percentage points more expensive at the import stage — a significant deterrent for bulk commercial importers

The Agriculture Infrastructure and Development Cess (AIDC) — introduced in Budget 2021 — was raised fivefold from 1% to 5%. AIDC proceeds are earmarked for financing agriculture infrastructure investments. The sharp cess hike makes this the highest AIDC rate applied to any imported commodity, reflecting the emergency nature of the forex conservation objective

Together, BCD (10%) + AIDC (5%) = 15% effective import duty — a 9 percentage point increase in a single announcement. Additionally, a 3% Integrated GST (IGST) is payable on imported gold and silver in addition to these basic duties. With IGST, the total levy on gold and silver at import rises to approximately 18% — one of the highest duty structures on precious metals globally

Platinum — used in industrial applications, catalytic converters, and as a secondary precious metal — attracts a flat 5.4% import duty. This differential treatment reflects the government’s priority to protect India’s jewellery-export-linked platinum import chain, which supports the MSME gems and jewellery sector in Gujarat, Maharashtra, and West Bengal

- The government has also increased import duty on gold and silver findings to 5% — findings are small components such as hooks, clamps, pins, and screws used to hold the whole or a part of a piece of jewellery in place

- These were previously imported largely duty-free — the new 5% duty on findings is intended to support domestic manufacturing of jewellery components and reduce the import of semi-processed goods that circumvent higher gold duties

- Together, all these measures are intended to help the country deal with global disruptions and challenges arising from the West Asia conflict — as explicitly stated in the official notification

Why Gold? — India’s Precious Metal Import Vulnerability

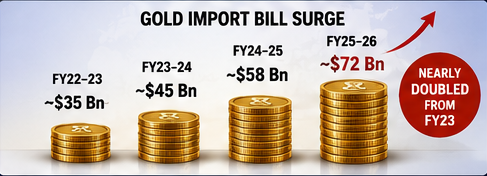

India is the world’s second-largest consumer of gold after China. Gold imports constitute the second-largest single item in India’s import bill — after crude oil — and are a primary driver of the Current Account Deficit (CAD). The import surge in FY26 has been particularly alarming:

| Financial Year | Gold Import Bill | Key Driver |

|---|---|---|

| FY2022–23 | $35 billion | Base year; moderate gold prices; stable rupee |

| FY2023–24 | ~$45 billion | Rising gold prices globally; increased investment demand |

| FY2024–25 | ~$58 billion | Gold prices hit record highs; wedding season demand surge |

| FY2025–26 | ~$72 billion | West Asia crisis → rupee fall → gold as safe haven → import surge; nearly doubled from FY23 |

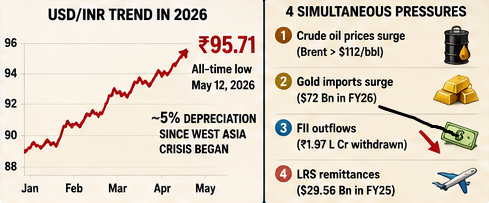

The Rupee at ₹95.71 — Understanding Currency Depreciation

The rupee closed at ₹95.71 to a US dollar on Wednesday, May 13, 2026 — its lowest-ever level. Since the beginning of the West Asia conflict, the rupee has lost approximately 5% of its value. Over the course of 2026 alone, it has fallen by nearly 5% against the US dollar — making it one of Asia’s weakest-performing currencies in 2026.

1. Crude oil import surge: Higher Brent prices (now $112+/bbl) means India needs more dollars to import the same volume of oil — dollar demand rises, rupee falls.

2. Gold imports: $72 Bn gold import bill creates enormous sustained demand for foreign exchange.

3. FII outflows: Foreign institutional investors withdrew ₹1.97 lakh crore (Jan–May 2026) from Indian equities amid geopolitical uncertainty — converting rupees into dollars, adding selling pressure.

4. LRS remittances: Outward remittances under LRS at $29.56 Bn in FY25 — foreign travel accounting for half — are a steady forex drain

A weaker rupee makes every import more expensive in rupee terms — raising inflation. Higher inflation pushes household savings toward gold (a traditional inflation hedge) — increasing gold imports further. More gold imports mean more forex outflow — weakening the rupee further. This depreciation → inflation → gold demand → more imports → more depreciation cycle is the spiral that the import duty hike is designed to break by raising the cost of entry into the cycle

Current Account Deficit (CAD) — The Core Economic Concern

The Current Account Deficit (CAD) is the difference between what India earns from the rest of the world (exports of goods, services, remittances received) and what it spends on the rest of the world (imports of goods and services). A persistently large CAD puts pressure on forex reserves and weakens the rupee — which is why the government is treating CAD management as a national priority in 2026.

- Crude oil (largest contributor): $174.9 Bn imports (22% of all imports, 88% imported) — addressed by PM Modi’s fuel conservation appeal and WFH guideline

- Gold (2nd largest contributor): $72 Bn imports (100% imported) — addressed by the new 15% import duty and PM’s appeal to avoid gold purchases for 1 year

- Outward LRS remittances: $29.56 Bn — addressed by PM’s appeal to postpone foreign travel for 1 year; government considering tighter TCS rules under LRS

- Edible oil: ~$15–20 Bn — addressed by PM’s guideline to reduce consumption; NMEO-Oil Palm for domestic production

- Goods exports: $437 Bn (FY26) — positive contribution; sugar export ban could modestly reduce export revenue short-term but is prioritised to protect domestic supply

The LRS — Liberalised Remittance Scheme — India’s Forex Safety Valve

The Liberalised Remittance Scheme (LRS) — introduced by the Reserve Bank of India in 2004 under the Foreign Exchange Management Act (FEMA), 1999 — allows every resident individual to remit up to USD 250,000 per financial year abroad for permitted transactions. It is one of the most significant controlled gateways for outward forex flow from India’s household sector.

| Feature | Detail |

|---|---|

| Annual limit | USD 250,000 per resident individual per financial year; applies to all resident individuals including minors (guardian must sign Form A2) |

| Who can use it | All resident individuals — NOT available to corporates, partnership firms, HUFs, or Trusts |

| Permitted uses | Foreign travel and accommodation; education fees abroad; medical treatment; gifts and donations; investment in foreign stocks, real estate; maintenance of relatives abroad |

| Prohibited uses | Margin trading; forex/cryptocurrency speculation; remittances to FATF-blacklisted countries; lottery winnings; racing/riding income |

| TCS (Tax Collected at Source) | No TCS up to ₹10 lakh/year (raised in Budget 2025 from ₹7 lakh); 5% TCS above ₹10 lakh (except education loans: 0% TCS); 20% TCS on overseas tour packages above ₹10 lakh |

| Documents required | Form A2 (RBI declaration); PAN Card (mandatory); KYC documents; purpose proof (university letter, hospital bills, flight tickets etc.) |

| Cash limit | Maximum USD 3,000 in physical cash; rest via forex cards, traveller’s cheques or direct transfers |

| FY25 LRS outflow | $29.56 billion total outward remittances; foreign travel accounted for more than half (~$15+ Bn) — India’s largest discretionary forex drain |

| Crisis context | Government’s primary demand-side tool: PM Modi’s Guideline 3 appeals to voluntarily postpone foreign travel for 1 year; additional tightening of TCS rates under discussion |

Historical Context — Gold Import Duty Changes in India

Impact Assessment — Winners and Losers

| Stakeholder | Impact | Short-term | Long-term |

|---|---|---|---|

| Consumers / Retail buyers | Gold and silver prices surge immediately | Gold crosses ₹1.64 lakh/10g; silver ₹3 lakh/kg; buying becomes significantly more expensive | Demand suppression over 12–18 months; shift toward gold bonds (SGB) |

| Gems & jewellery exporters | Higher input costs (imported gold) hurt margins | Export competitiveness reduced; cancelled orders possible; MSME sector stress | Offset if rupee stabilises and global gold demand stays elevated |

| Bullion importers / banks | Import volumes fall sharply | Banks authorised to import gold reduce orders; spot market tightens | Grey market / smuggling risk rises if duty persists — same as 2012–14 episode |

| Rupee & forex reserves | Direct positive: reduces forex outflow | Immediate rupee support; import bill falls by estimated $15–20 Bn if gold imports halve | Sustained CAD improvement; reserve rebuild over 2–3 quarters |

| Government revenue | Higher duty = higher customs collection | Revenue from 15% duty on reduced volume; net impact positive on collection | Reduced volume partially offsets higher rate; AIDC cess earmarked for agriculture |

| SGB investors | Paper gold becomes relatively more attractive | SGB demand expected to surge as physical gold prices hit new highs | Supports government’s long-term agenda of reducing physical gold import dependence |

Prelims Question

1. The new effective import duty on gold and silver in India comprises a 10% Basic Customs Duty (BCD) and a 5% Agriculture Infrastructure and Development Cess (AIDC), totalling 15%.

2. The Agriculture Infrastructure and Development Cess (AIDC), introduced in the Union Budget 2021, is a cess whose proceeds are constitutionally mandated to be shared with state governments.

3. Under the Liberalised Remittance Scheme (LRS), resident individuals can remit up to USD 250,000 per financial year for both current account transactions (such as travel and education) and capital account transactions (such as foreign investment).

4. The LRS is available to all resident individuals including minors, but is not available to corporates, partnership firms, HUFs, or Trusts.

Which of the statements given above are correct?

Statement 1 is CORRECT. The midnight announcement of May 13, 2026 raised the Basic Customs Duty (BCD) on gold and silver from 5% to 10%, and the Agriculture Infrastructure and Development Cess (AIDC) from 1% to 5% — resulting in a total effective import duty of 15%, up from the earlier 6%. Additionally, a 3% Integrated GST (IGST) is payable on top of these components, taking the total import tax burden on gold to approximately 18%.

Statement 2 is INCORRECT. This is a critical constitutional distinction. The AIDC is a cess — not a tax. Under Article 270 of the Constitution, taxes collected into the Consolidated Fund of India are shared with states through the Finance Commission’s devolution formula. However, cesses and surcharges are explicitly excluded from the divisible pool — they accrue entirely to the Union Government and are not shared with states. The AIDC was introduced precisely as a cess (rather than a customs duty) so that its entire proceeds remain with the Centre to fund agriculture infrastructure without triggering state-sharing obligations. Several states have objected to this practice as it erodes the devolution they receive.

Statement 3 is CORRECT. The Liberalised Remittance Scheme, introduced by the RBI in 2004 under FEMA 1999, permits Indian resident individuals to remit up to USD 250,000 per financial year (April 1 to March 31) for a combination of permitted current account transactions (foreign travel, education fees, medical treatment, gifts) and capital account transactions (investment in foreign stocks, real estate, or overseas bank accounts). The $29.56 billion outward remittances in FY25 — of which travel accounted for more than half — are the scale of this outflow.

Statement 4 is CORRECT. The LRS is explicitly available only to resident individuals — including minors (provided a guardian signs Form A2). It is categorically NOT available to non-individual entities: corporates, partnership firms, Hindu Undivided Families (HUFs), and Trusts are excluded from using LRS. This individual-specific design was intentional — to allow personal financial freedom while preventing institutional-scale capital flight through a liberal individual window.

Mains Questions

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments