Achievements under the Scheme

The total number of farmers enrolled has increased from 3.17 crore in 2022-23 to 4.19 crore in 2024-25, i.e. an increase of 32%.

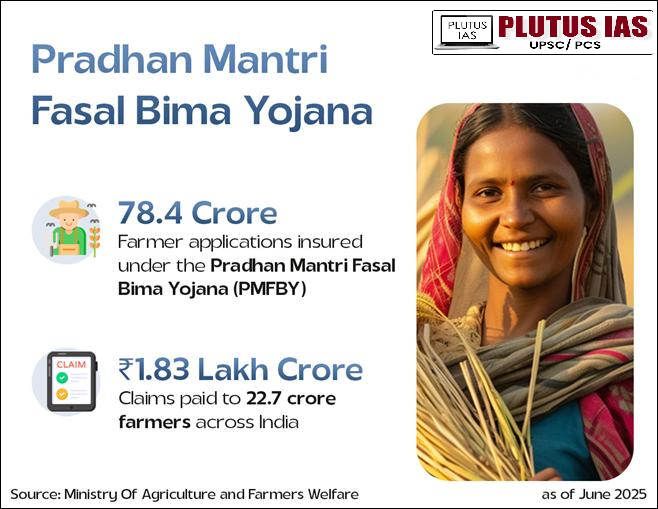

Since inception in 2016 till 2024-25 (as on 30.06.2025), a total of 78.407 crore farmer applications have been insured under PMFBY.

Out of these applications, 22.667 crore farmers received claims totaling₹1.83 lakh crore.

As compared to erstwhile crop insurance schemes, coverage of farmer applications has increased from 371 lakh in 2014-15 to 1510 lakh in 2024-25.

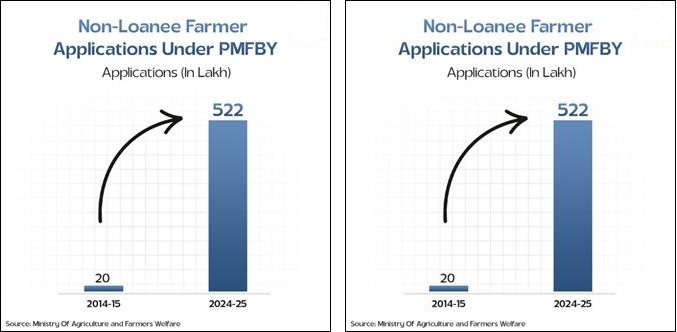

The number of non-loanee farmer applications has increased from 20 lakh in 2014-15 to 522 lakh in 2024-25.

Witnessing the success and potential of the scheme, the Union Cabinet in January 2025 approved the continuation of Pradhan Mantri Fasal Bima Yojana and Restructured Weather-Based Crop Insurance Scheme till 2025-26 with a total budget of ₹69,515.71 crore.

Strengthening the Pradhan Mantri Fasal Bima Yojana

Since its launch in 2016, the Government has undertaken several measures to strengthen the Pradhan Mantri Fasal Bima Yojana (PMFBY), with a focus on enhancing transparency, accountability and timely settlement of claims. These efforts have led to significant improvements in the scheme’s implementation.

As a result, both the area covered and the number of farmers enrolled have reached record levels in 2024–25. A total of 4.19 crore farmers have been enrolled under the scheme, marking the highest enrolment since inception. Out of the total farmer applications enrolled under the scheme in 2024-25,6.5%, 17.6% and 48% are pertaining to tenant, marginal and loanee farmers, respectively.

PMFBY is now the largest crop insurance scheme in the world in terms of farmer applications. In addition, several States have waived the farmer’s share of the premium, significantly reducing the financial burden on farmers and encouraging wider participation in the scheme.

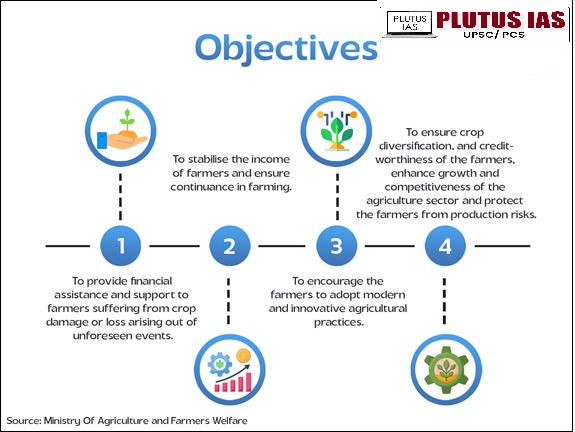

Objectives

Benefits

1. Affordable Premiums: The maximum premium payable by the farmer will be 2% for the Kharif food and oilseed crops. For rabi food and oilseeds crop, it is 1.5% and for yearly commercial or horticultural crops, it will be 5%. The remaining part (95% to 98.5%) of the actuarial premium is borne jointly by the Central and State Governments on a 50:50 basis, except for North Eastern States (from Kharif 2020) and Himalayan States (from Kharif 2023) where it is shared in the ratio of 90:10.

2. Comprehensive Coverage: The scheme covers natural disasters (droughts, floods), pests, and diseases. Post-harvest losses due to local risks like hailstorms and landslides are also included.

3. Timely Compensation: PMFBY aims to process claims within two months of the harvest to ensure that farmers get the compensation quickly, preventing them from falling into debt traps.

4. Technology-Driven Implementation: PMFBY integrates advanced technologies like satellite imaging, drones, and mobile apps for precise estimation of crop loss, ensuring accurate claim settlements.

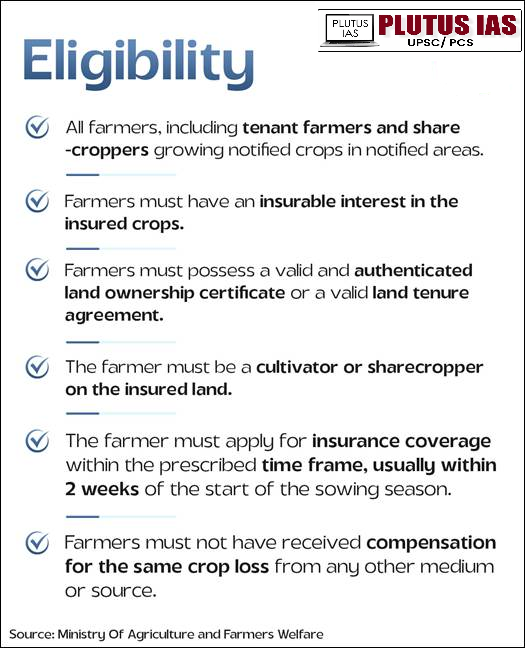

Eligibility

| Category |

Eligibility |

Enrollment |

Special Notes |

| Non-Loanee Farmers |

– Farmers with non-standard KCC scheme-linked crop loans

– Farmers who have not taken any crop loans |

Voluntary enrollment under PMFBY to mitigate risk and claim insurance benefits |

Includes all farmers without crop loans; can join PMFBY on their own |

| Loanee Farmers |

– Farmers sanctioned loans from financial institutions (FIs) for Seasonal Agricultural Operations (SAO) |

Mandatory enrollment under PMFBY |

Premiums deducted from SAO crop loans; crop loans against collateral like fixed deposits, gold/jewel loans, or mortgage loans without insurable interest on the land are not covered |

Risks Covered

1. Yield Losses (Standing Crops): The Government provides this insurance coverage for yield losses that fall under the non-preventable risks, such as Natural Fire and Lightning, Storm, Hailstorm, Tornado etc.; Flood, Inundation and Landslide; Pests/ Diseases, etc.; Drought etc.

2. Prevented Sowing: Cases may arise where most of the farmers (insured) of notified areas may want to plant or sow. In such cases, they have to bear the expenditure for that cause and are restricted from planting or sowing insured crops because of unfavorable weather conditions. These farmers will then become eligible for the indemnity claims of up to a maximum of 25% of the sum insured.

3. Post-harvest Losses: The Government provides for post-harvest losses on an individual farm basis. The Government offers coverage of up to 14 days (maximum) from harvesting for crops that are stored in “cut and spread” condition. It means that the Government covers farmers who have put the crops to become sun-baked in the field after harvesting, which have been destroyed due to cyclone or cyclonic rains occurred across the country.

4. Localised Calamities: The Government provides for localised calamities on an individual farm basis. Risks such as loss or damage arising from identified localised hazards, such as hailstorms, landslides, and inundation impacting separated farmlands in the notified area come under this coverage.

Key Government Initiatives to Strengthen PMFBY Implementation

| Initiative |

Description |

Impact |

| National Crop Insurance Portal (NCIP) |

Online farmer enrolment, data sharing, monitoring, and direct transfer of claims |

Improves transparency, speeds up claim settlement |

| Digi Claim Module (from Kharif 2022) |

Links NCIP with PFMS and insurance company systems; auto 12% penalty for delayed claims (from Kharif 2024) |

Ensures timely payment, penalises delays |

| Separate Central Premium Subsidy |

Central share of premium subsidy released directly, independent of the State share |

Farmers receive claims faster |

| Mandatory ESCROW Account (from Kharif 2025) |

States must deposit the premium share in advance |

Avoids delays in claim processing |

| Technology Integration |

CCE-Agri mobile app for yield data; State land records linked to NCIP; insurers attend CCEs |

Enhances accuracy, reduces disputes |

| Awareness Drives |

Campaigns by States, insurers, banks, CSCs, PRIs to promote PMFBY |

Increases farmer participation |

| Crop Insurance Week / Fasal Bima Saptah |

Bi-annual awareness week (from Kharif 2021) with village-level Fasal Bima Pathshalas |

Educates farmers at the grassroots level |

| Meri Policy Mere Haath |

Special camps to distribute crop insurance policy receipts at the village/GP level |

Improves access to policy details |

| KRPH – KrishiRakshak Portal & Helpline (14447) |

An online portal and a toll-free number for grievances with ticket tracking |

Strengthens the grievance redressal system |

Application Process

Conclusion

The Pradhan Mantri Fasal Bima Yojana (PMFBY) has transformed India’s agricultural safety net by providing affordable premiums and extensive risk coverage, including yield losses, post-harvest losses and localized calamities. The scheme ensures timely compensation and stabilises farmers’ income. By adopting advanced technologies such as satellite imagery, drones, mobile data capture and weather monitoring, PMFBY has improved transparency, accuracy and efficiency in crop loss assessment. Growing participation of non-loanee and marginal farmers reflects the increasing trust in the scheme.

Source: PIB

Prelims Questions

No Comments