India’s economic ascent continues to capture global attention. Already the world’s fourth largest economy, the nation is charting a confident course toward becoming the third largest by 2030, with GDP projected at USD 7.3 trillion. The current growth phase reflects the strength of decisive policymaking, structural reforms, and India’s deepening global integration.

With growth accelerating, India has once again outpaced global peers, reinforcing its position as the fastest-growing major economy. The surge is supported by resilient domestic demand, moderating inflation, and higher labour force participation. A revival in domestic investment and strong investor sentiment signals a stable and broad-based economy. As reforms gather pace and consumption remains optimistic, India’s economic outlook continues to upbeat, signalling sustained momentum and growth across sectors.

Key Economic Indicators: India’s Steady and Resilient Growth

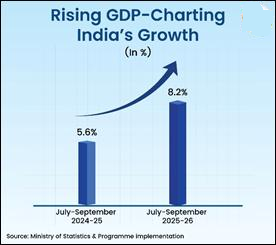

Robust GDP Performance

Gross Domestic Product (GDP) remains the central measure of economic health, reflecting how rapidly the economy is expanding. As per the latest data, India’s real GDP grew by 8.2% in Q2 of FY 2025–26, a significant rise from 5.6% in Q2 of FY 2024–25. In Q1 of FY 2025–26, real GDP grew by 7.8%, compared to 6.5% in the previous year.

Nominal GDP growth stood at 8.7% in Q2 FY 2025–26. Each major sector contributed positively:

Primary Sector: 3.1%

Secondary Sector: 8.1%

Tertiary Sector: 9.2%

Overall, India recorded 8% H1 (Apr–Sep 2025–26) growth, higher than 6.1% in H1 FY 2024–25, with the secondary and tertiary sectors showing strong and sustained expansion.

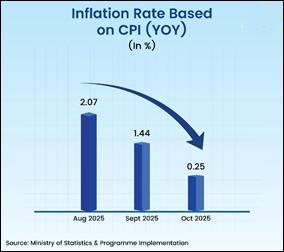

Inflation Shows Stability and Improvement

India’s inflation trends in October 2025 demonstrate strong macroeconomic management. Headline inflation (CPI) eased sharply to 0.25%, the lowest in the current CPI series, and comfortably within the RBI’s tolerance band. This aligns with the RBI’s decision to maintain the repo rate at 5.50% with a neutral stance.

| Indicator |

September 2025 |

October 2025 |

| CPI |

1.44 |

0.25 |

| CFPI |

–2.33 |

–5.02 |

| Rural Inflation |

1.07 |

–0.25 |

| Urban Inflation |

1.83 |

0.88 |

This sharp moderation was largely driven by lower food prices—vegetables, oils, fruits, eggs, and cereals—along with the positive impact of GST rate cuts.

Wholesale inflation (WPI) also declined to –1.21% in October 2025, supported by lower prices of crude petroleum, natural gas, electricity, and metal products. The WPI Food Index fell to –5.04%, signalling stronger purchasing power for producers and businesses.

Industrial Activity Picks Up: Strong IIP Growth

The Index of Industrial Production (IIP), a key measure of manufacturing and mining performance, grew by 4.0% in September 2025. Manufacturing output rose by 4.8%, driven by:

Basic Metals: 12.3%

Electrical Equipment: 28.7%

Motor Vehicles & Trailers: 14.6%

Use-based categories also posted strong increases:

Infrastructure & Construction Goods: 10.5%

Consumer Durables: 10.2%

Intermediate Goods: 5.3%

This balanced industrial improvement reflects rising consumption, expanding investment, and a broad-based manufacturing recovery.

Manufacturing Sector Strengthened by Government Interventions

Manufacturing has become a central pillar of India’s growth model. The Production Linked Incentive (PLI) Scheme remains a major driver, covering 14 strategic sectors and aiming to boost domestic capacity, exports, and jobs.

Approved outlay: ₹1.97 lakh crore

Investments attracted: ₹1.76 lakh crore

Applications approved: 800+

Complementary initiatives like Make in India, Skill India, National Manufacturing Mission, and GST reforms have built a strong and competitive manufacturing ecosystem integrated with global value chains.

Employment & Labour Market Indicators (October 2025)

| Category |

Indicator / Data |

Value / Details |

| Labour Market Performance (CWS) |

Labour Force Participation Rate (LFPR) |

55.4% (highest in 6 months) |

|

Worker Participation Rate (WPR) |

52.5% |

|

Female LFPR |

34.2% (highest since May 2025) |

|

Unemployment Rate |

5.2% |

| Formal Employment |

EPFO Net Additions (July 2025) |

21.04 lakh |

|

YoY Growth |

5.55% increase |

| White-Collar Hiring (Naukri JobSpeak Index) |

Overall YoY hiring growth |

10.1% |

|

AI & ML job roles |

61% increase |

|

Fresher hiring |

15% increase |

| Government Skill & Employment Programs |

PMKVY (Skilling) |

27 lakh candidates trained |

|

NAVYA |

Skilling adolescent girls for emerging sectors |

|

PMMY |

₹4.91 lakh crore sanctioned |

|

Stand-Up India |

₹62,790 crore sanctioned |

|

Start-Up India |

2.00 lakh recognised startups |

| Rozgar Mela |

Latest Edition |

17th Rozgar Mela |

|

Appointment Letters Distributed |

51,000 |

India’s Trade Performance Strengthens

1. Exports (Merchandise + Services)

USD 491.80 billion, up 4.84% from last year

2. Merchandise Exports:

USD 254.25 billion, growing despite global uncertainties

Key markets: Spain, China, Hong Kong, USA, UAE

Strong categories: Electronic Goods (37.82%), Cashew (28.32%), Marine Products (16.18%)

3. Services Exports:

USD 237.55 billion, up 9.75%

Driven by computer services, business services, and digital trade

4. Trade Facilitation Measures

Extended export value realisation period to 15 months

Shipment time extended to 3 years

Credit Guarantee Scheme for Exporters: Coverage up to ₹20,000 crore

Export Promotion Mission: Outlay of ₹25,060 crore (2025–31)

Initiatives like RoDTEP, SEZ reforms, and Districts as Export Hubs support diversification and logistics efficiency.

Success of GST 2.0

GST 2.0 introduced a simplified two-slab structure (5% and 18%) with significant rate rationalisation across essential goods and labour-intensive sectors.

GST collections (Oct 2025): ₹1.96 lakh crore

YoY increase: 4.6%

Lower rates have boosted consumption, reduced compliance burden, and expanded the tax base, ensuring sustainable revenue generation.

India’s Growth Projections Improve

Global institutions reflect growing confidence in India’s economic performance:

RBI: Upgraded FY26 forecast from 6.5% → 6.8%

World Bank: 6.5% (2026)

Moody’s: 6.4% (2026), 6.5% (2027)

IMF: 6.6% (2025), 6.2% (2026)

OECD: 6.7% (2025), 6.2% (2026)

S&P: 6.5% (FY26), 6.7% (2027)

Conclusion

India’s economy continues to advance on a stable, resilient, and inclusive growth path, supported by structural reforms, digitalisation, improved ease of doing business, and robust policy frameworks. With inflation well-anchored, employment improving, manufacturing accelerating, and global institutions expressing confidence in India’s trajectory, the country is well-positioned to sustain its momentum in the coming years. Government initiatives—ranging from GST simplification and employment generation to export promotion and industrial policy—are making the economy more competitive, productive, and people-centric. Together, these trends underscore India’s evolving strength as a major global economic powerhouse.

No Comments