13 May Minister Puri Hints at Fuel Price Hike

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS Paper 3 : Economy , IR

FOR PRELIMS : Under-Recoveries , OMCs , Strategic Petroleum Reserve

FOR MAINS : “India’s petroleum pricing policy reflects a broader governance failure — the capture of public enterprises by electoral politics, where companies that should function as commercial entities are instead used as instruments of populist price management.” Analyse this argument with reference to the historical functioning of OMCs, the problem of under-recoveries, and the reforms needed to make India’s petroleum sector genuinely market-driven. (15 M)

Why in News?

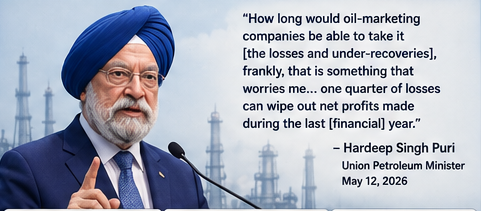

Addressing theConfederation of Indian Industries (CII) Annual Business Summit on May 12, 2026, Union Petroleum MinisterHardeep Singh Puriissued the starkest public warning yet about the financial condition of India’s oil marketing companies (OMCs), stating thatIndia’s three state-owned OMCs are collectively losing ₹1,000 crore every single daydue to selling petrol, diesel, and LPG below market cost. Cumulativeunder-recoveries have climbed to ₹1.98 lakh crorethis quarter — and a single quarter of losses of₹1 lakh crore could wipe out the entire annual profits earned by OMCs last year. While ruling out an imminent price hike and affirming that India has60 days of crude oil stocks, 60 days of LNG, and 45 days of LPG, the Minister raised the pointed question:“How long would oil-marketing companies be able to take it [the losses and under-recoveries]?”— a signal widely interpreted by markets as preparing the ground for an eventual fuel price revision.

What Are Under-Recoveries? — Understanding the Core Concept

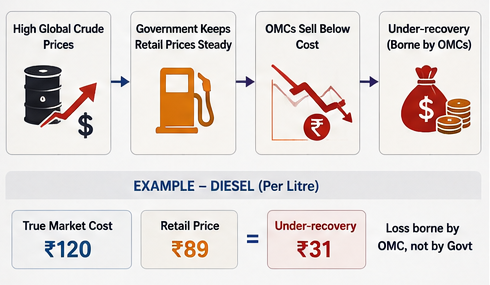

Under-recovery is a term specific to India’s petroleum sector. It refers to the difference between the internationally benchmarked cost of producing and importing a fuel and the actual price at which OMCs sell it to consumers at the retail pump. When global crude oil prices rise but domestic retail prices are held steady by the government (for political or welfare reasons), OMCs are forced to sell fuel below their cost of procurement — “recovering” less than they spent. This is an implicit subsidy borne by the companies, not the government’s budget directly.

If the true market cost of producing 1 litre of diesel is ₹120 but the government-influenced retail price is ₹89, the OMC “under-recovers” ₹31 per litre — this is a loss borne by the company, not reimbursed by the government

A subsidy appears in the government budget — the government pays the company the difference. An under-recovery does not appear in the budget — the company itself absorbs the loss, which erodes its profits, equity, and borrowing capacity. Under-recoveries are thus a hidden, off-budget burden on public sector enterprises

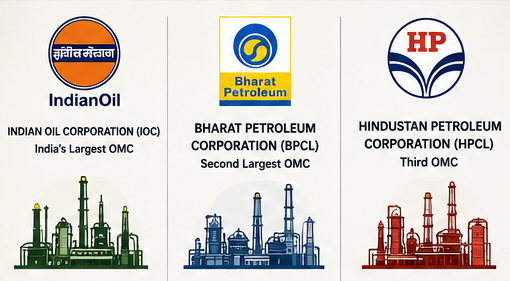

India’s Three OMCs — Who Are They?

Refines and markets petrol, diesel, LPG, aviation fuel, lubricants. Operates India’s largest refinery network (~11 refineries). IOC accounts for approximately49% of India’s petroleum product sales. Largest contributor to OMC under-recoveries. Listed on BSE/NSE; government holds ~51.5%

Operates major refineries in Mumbai, Kochi, and Bina. Significant LPG distribution network. The government’s earlier disinvestment attempt (2020–2022) was abandoned.Government holds ~52.98%; BPCL’s private equity and retail fuel operations are a critical national asset

Refineries in Mumbai and Visakhapatnam; extensive retail network.ONGC acquired majority stake (54.9%) in HPCL in 2018. Significant LPG bottling and distribution capacity; the West Asia crisis impacts HPCL’s Vizag refinery most directly due to its reliance on Middle Eastern crude grades

How OMC Losses Have Evolved — Historical Context

The Supply Side — India’s Fuel Buffer

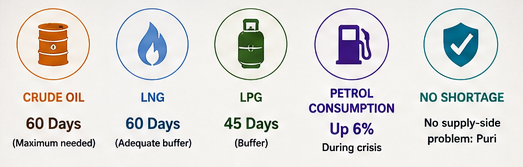

Despite the financial stress on OMCs, Minister Puri was emphatic on the supply side:“There is no problem on supply management side, there is no shortage anywhere.”India began the West Asia crisis with stronger-than-usual stockpiles, and has actively managed supply since the Strait of Hormuz closure.

| Fuel Type | Current Stockpile / Situation | Normal Buffer | Action Taken |

|---|---|---|---|

| Crude oil | 60 days (maximum needed) | 30–45 days typically | Strategic Petroleum Reserve (SPR) at Visakhapatnam, Padur, and Mangalore deployed; alternative sourcing from Russia, United States, and Canada activated |

| LNG (Liquefied Natural Gas) | 60 days | 30 days typically | Spot LNG purchases from alternative suppliers after the Ras Laffan strike; energy consumption rose 6% during the crisis |

| LPG (Cooking gas) | 45 days | 30 days | Domestic LPG production ramped from 35,000–36,000 MT/day to 54,000 MT/day — a 50%+ production surge to offset import disruptions |

| Petrol consumption | Consumption up 6% during crisis | N/A | Consumption rose despite conservation appeals, highlighting limits of voluntary austerity |

Fuel Price History — The Political Economy of Petrol Prices

| Period | Retail Fuel Policy | Brent Crude (Approx.) | OMC Financial Health |

|---|---|---|---|

| 2010–2014 | Administered pricing; massive under-recoveries; oil bonds issued | $80–$110/bbl | Heavy losses; chronic under-recoveries exceeding ₹1 lakh crore/year |

| 2014–2016 | Diesel deregulated (Oct 2014); falling oil prices eased transition | $26–$55/bbl | Strong profits; over-recoveries; healthy margins |

| 2017–2021 | Technically deregulated; prices revised frequently but often frozen near elections | $40–$75/bbl | Moderate-to-good margins; generally profitable |

| 2022 (Mar–May) | Last major fuel price hike — petrol and diesel up ₹8–10/litre; LPG prices raised | $100–$120/bbl | Losses before hikes; margins improved afterward |

| 2022–2026 | Four-year price freeze despite crude fluctuations | $65–$90/bbl (pre-war) | FY25 profits around ₹1 lakh crore combined |

| Feb–May 2026 | Prices still frozen despite 55% crude surge; diesel excise duty cut to zero | $112–$130/bbl | Losses of ~₹1,000 crore/day; quarterly under-recoveries of ₹1.98 lakh crore |

The Trilemma Facing the Government

The government faces a classic energy policy trilemma — it cannot simultaneously achieve all three goals at once. It must choose which two to prioritise:

- Goal 1 — Affordable fuel for consumers: Keep petrol, diesel, and LPG prices low to protect household budgets, control inflation, and maintain political support; directly conflicts with OMC financial health at current crude prices

- Goal 2 — OMC financial sustainability: Allow OMCs to recover costs and remain profitable enough to invest in refining capacity, pipelines, and future energy transition; directly conflicts with affordable prices when crude is above $100/bbl

- Goal 3 — Fiscal discipline: Avoid compensating OMCs from the budget (which would widen the fiscal deficit); avoid raising excise duties (which would reverse the Modi government’s 2026 duty cut); directly in tension with both goals above

Currently, the government is prioritising Goal 1 (consumer affordability) at the expense of Goal 2 (OMC health), while trying to manage Goal 3 through excise duty cuts on pump prices (sacrificing revenue to control retail prices). This is fiscally expensive and operationally unsustainable — exactly what Puri’s CII speech was signalling.

Policy Options Before the Government

| Option | Mechanism | Pros | Cons |

|---|---|---|---|

| Retail fuel price hike | Allow OMCs to raise petrol, diesel, and LPG prices at the pump | Directly restores OMC margins; most financially effective; market-consistent | Politically costly; increases retail inflation; disproportionately impacts lower-income households; contradicts austerity messaging |

| Budget compensation (oil bonds) | Government reimburses OMC losses through cash transfers or bonds | Keeps consumer prices low; protects OMC balance sheets | Widens fiscal deficit; shifts burden to taxpayers; creates moral hazard; revives the discredited “oil bond” model |

| Excise duty structure change | Reduce central excise further or restructure state VAT on fuels | Reduces consumer burden without hurting OMCs; can be revenue-neutral if calibrated carefully | Further reduces government revenue; coordination with states on VAT is difficult; limited room left after April 2026 cuts |

| Targeted LPG subsidy (DBT) | Raise LPG prices while compensating only BPL households via direct benefit transfer | Progressive and fiscally efficient; restores OMC margins while protecting vulnerable households | Middle-class backlash likely; DBT infrastructure requires expansion; many urban LPG users remain outside subsidy coverage |

| Staged gradual hike | Introduce small monthly fuel price increases of ₹1–2/litre over 6–12 months | Minimises political shock; allows consumers to adjust gradually; reduces inflationary base effects | OMC losses continue in the short term; requires sustained political commitment; vulnerable to opposition criticism |

Strategic Petroleum Reserve (SPR) — India’s Buffer Against Shocks

India’s Strategic Petroleum Reserve — created after the oil shocks of the 2000s — is managed by the Indian Strategic Petroleum Reserves Limited (ISPRL) under the Ministry of Petroleum. It currently stores crude oil at three underground rock cavern facilities:

- Vishakhapatnam (Andhra Pradesh): 1.33 million tonnes capacity — largest facility; operational since 2016

- Mangalore (Karnataka): 1.5 million tonnes capacity; operational; second facility

- Padur (Karnataka): 2.5 million tonnes capacity — largest of the three; partially operational

Prelims Question

1. Under-recovery is the difference between the internationally benchmarked cost of a petroleum product and the actual retail price at which OMCs sell it to consumers — it represents a loss borne by the company, not the government budget directly.

2. India’s three major OMCs — IOC, BPCL, and HPCL — are all Maharatna category Public Sector Undertakings under the Ministry of Petroleum and Natural Gas.

3. India’s Strategic Petroleum Reserve is managed by Indian Strategic Petroleum Reserves Limited (ISPRL) and is stored in underground rock cavern facilities at Vishakhapatnam, Mangalore, and Padur.

4. The Petroleum and Natural Gas Regulatory Board (PNGRB) directly sets the retail prices of petrol and diesel in India and must approve any price revision by OMCs.

Which of the statements given above are correct?

Statement 1 is CORRECT. Under-recovery is precisely the gap between what the fuel costs OMCs (based on international benchmark prices) and what they charge consumers at the pump. Unlike a formal government subsidy that appears on the budget, under-recovery is absorbed by the company itself — eroding its profits, balance sheet, and investment capacity. This is why the ₹1.98 lakh crore under-recovery in Q1 FY27 directly threatens OMC financial viability without automatically showing up as a government expenditure.

Statement 2 is INCORRECT. Not all three OMCs are Maharatna PSUs. Indian Oil Corporation (IOC) and Bharat Petroleum (BPCL) are Maharatna PSUs. However, HPCL (Hindustan Petroleum Corporation Ltd) is a Navratna PSU — not a Maharatna. HPCL became a subsidiary of ONGC when ONGC acquired a 54.9% stake in 2018. HPCL has not yet been upgraded to Maharatna status as of 2026. This is a classic UPSC-style factual distinction.

Statement 3 is CORRECT. India’s Strategic Petroleum Reserve is indeed managed by ISPRL (Indian Strategic Petroleum Reserves Limited), a Special Purpose Vehicle under the Ministry of Petroleum. The three underground rock cavern facilities are at Vishakhapatnam (1.33 MT, Andhra Pradesh), Mangalore (1.5 MT, Karnataka), and Padur (2.5 MT, Karnataka) — giving a combined capacity of approximately 5.33 million tonnes. Minister Puri’s “60 days of crude” figure includes both this SPR and OMC commercial inventory.

Statement 4 is INCORRECT. The PNGRB does not set retail petrol and diesel prices. Petrol was deregulated in 2010 and diesel in October 2014 — meaning OMCs are technically free to set prices based on market costs without PNGRB approval. In practice, the government exerts political pressure on OMCs not to raise prices. PNGRB’s mandate covers regulation of natural gas pipelines, city gas distribution networks, and LNG terminals — not retail auto-fuel pricing.

Mains Questions

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments