25 Apr Payments Banks: Bridging Inclusion or Breaching Regulation?

This article covers “Daily Current Affairs”

SYLLABUS MAPPING : GS 3 : Economy

FOR PRELIMS : Various Banking Committees , Payment Banks Regulations , Payment Banks Features

FOR MAINS : “Payments Banks were envisioned as instruments of financial inclusion, but recent regulatory actions raise concerns about their governance and sustainability.” Discuss in the context of the Paytm Payments Bank licence cancellation.

Why in News? (24/04/26)

RBI invoked Section 22(4) of the Banking Regulation Act, 1949 to cancel Paytm Payments Bank Ltd’s licence with immediate effect. The central bank will approach the High Court to initiate winding-up proceedings. PPBL holds sufficient liquidity to repay all deposit liabilities in full.

Regulatory action timeline

RBI conducts onboarding audit. Finds significant KYC gaps: a single PAN linked to multiple customer accounts; transactions beyond prescribed limits. Bank directed to stop onboarding new customers.

After PPBL failed to address compliance concerns, RBI formally reissues the restriction on onboarding new customers. Compliance failures persist for over 4 years.

RBI imposes a monetary penalty of ₹5.39 crore on PPBL for regulatory violations.

RBI bars PPBL from accepting any further deposits, credits, or top-ups across all accounts, wallets, FASTags, and NCMC cards — effective February 29, 2024. This effectively cripples core operations.

Further business restrictions imposed. PPBL operations severely curtailed. One97 Communications writes off its PPBL investment.

RBI cancels banking licence under §22(4). Winding-up via High Court ordered. PPBL prohibited from all banking activities under Banking Regulation Act, 1949.

Reasons for cancellation

One of RBI’s most flagged issues: PPBL linked a single Permanent Account Number (PAN) to multiple customer accounts — a direct violation of KYC norms. This created serious concerns about potential money laundering and circumvention of transaction limits.

Customers were allowed to transact beyond the regulatory ceilings prescribed for payments banks, undermining the prudential framework designed to limit risk exposure.

PPBL failed to maintain the mandatory operational separation between itself and its group company One97 Communications. This blurring of boundaries violated core governance and conflict-of-interest requirements under banking law.

RBI explicitly stated: “The general character of the management of the bank is prejudicial to the interest of depositors as also the public interest…no useful purpose or public interest would be served by allowing the bank to continue.”

Despite being under scrutiny since 2018 — including customer onboarding bans, financial penalties, and deposit restrictions — PPBL failed to rectify fundamental compliance failures over 8 years, leaving the RBI no option but cancellation.

In June 2018, an RBI audit found significant gaps in onboarding processes and AML (anti-money laundering) controls. The bank was found to not consistently follow proper KYC procedures during new customer acquisition.

What happens now?

Depositors are safe

RBI has confirmed PPBL holds sufficient liquidity to repay all deposit liabilities in full. The winding-up process — supervised by the High Court — will determine the timeline for returning customer funds.

Paytm app continues

One97 Communications clarified it has no financial exposure to PPBL (written off in March 2024). The Paytm app, Paytm UPI, QR codes, Soundbox, card machines, and Paytm Money continue to operate independently of PPBL.

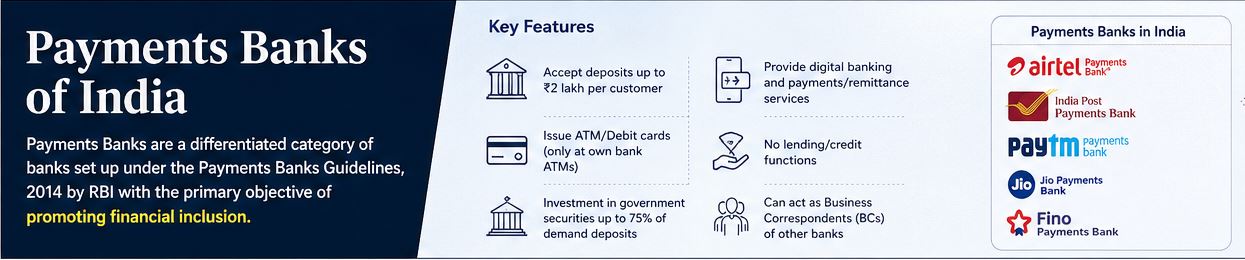

Payments Banks Creation in India

The financial inclusion gap

Despite decades of bank nationalisation (1969, 1980), over 40% of India’s adult population remained unbanked by 2013. Migrant workers, daily-wage earners, and rural households lacked safe channels for deposits and remittances. Traditional banks found serving them commercially unviable.

Evolution — key milestones

RBI forms the Committee on Comprehensive Financial Services. Recommends a new category of “differentiated banks” focused purely on payments and deposits — not credit.

Mor Committee submits its report. Concept of Payments Banks formally proposed as a vehicle for last-mile financial inclusion.

Draft guidelines released for public comment. Core features crystallised: deposit ceiling, investment mandate, ban on lending.

RBI grants in-principle approval to 11 applicants out of 41, including Airtel, Paytm, Reliance, India Post, Vodafone M-Pesa, Fino, NSDL, Aditya Birla, Tech Mahindra, Department of Posts, and National Securities Depository.

Airtel Payments Bank becomes India’s first operational payments bank.

Vodafone M-Pesa, Aditya Birla, and Tech Mahindra surrender licences citing unviable business model. Only 6 remain operational.

RBI cancels PPBL’s banking licence under Section 22(4) of Banking Regulation Act, 1949 — orders winding up via High Court. Now only 5 payments banks operational.

Governing legal framework

| Primary legislation | Banking Regulation Act, 1949 (licence under §22) |

| Regulatory authority | Reserve Bank of India (RBI) |

| Additional statutes | RBI Act 1934 · Companies Act 2013 · FEMA 1999 · PSS Act 2007 |

| Legal structure | Must be incorporated as a Public Limited Company |

| Minimum capital | ₹100 crore paid-up equity capital |

| Promoter lock-in | Min. 40% stake for first 5 years |

| CAR requirement | 15% of Risk-Weighted Assets (Tier I ≥ 7.5%) |

What can Payments Banks do?

Permitted

- Accept demand deposits (savings + current) up to ₹2 lakh per customer.

- Issue debit cards (not credit cards)

- Provide internet & mobile banking

- Enable remittances and cross-border transfers (current accounts)

- Invest 75% of demand deposits in govt. securities (SLR-eligible).

- Park remaining 25% as time deposits with other scheduled commercial banks.

- Distribute third-party products: insurance, mutual funds, pension schemes.

- Issue prepaid payment instruments (PPIs) and FASTags

Prohibited

- Grant loans, advances or overdrafts

- Issue credit cards

- Accept NRI deposits or time deposits

- Set up subsidiaries for NBFC activities

- Accept deposits exceeding ₹2 lakh per customer.

- Participate in the inter-bank call money market as lenders.

- Invest beyond government securities for the 75% SLR portion

Currently operational payments banks (post-Paytm cancellation)

Structural challenges of payments banks

Challenge 1

The prohibition on issuing loans or credit fundamentally limits revenue. Earnings depend on thin float income from G-sec investments, transaction fees, and third-party commissions. Most payments banks have struggled to turn a profit. Economists like S. Kalyanasundaram (EPW, 2020) have called the model structurally unviable.

Challenge 2

The ₹2 lakh deposit cap (raised from ₹1 lakh by RBI) limits the float that payments banks can build. High-value customers gravitate to full-service banks. This ceiling simultaneously protects depositors but constrains business viability.

Challenge 3

The Paytm case illustrates that digital-first onboarding at scale creates compliance risks. Managing KYC for millions of low-income, semi-literate customers while meeting RBI’s norms on AML, transaction limits, and data integrity is operationally demanding and costly.

Challenge 4

Payments banks must invest 75% of their demand deposits in government securities. While safe, the returns are modest. The remaining 25% is parked as time deposits with other banks — not deployed in higher-yield assets.

Challenge 5

With PhonePe, Google Pay, and other non-bank payment players offering near-identical payment services without the regulatory burden of a banking licence, payments banks face competition from entities that are not subject to the same capital, KYC, or reporting requirements.

Challenge 6

Despite their financial inclusion mandate, reaching truly unbanked populations in remote rural areas requires physical agent networks and financial literacy investments that erode already thin margins. India Post Payments Bank faces this challenge most acutely despite leveraging 1.55 lakh post offices.

Challenge 7

Of the 11 licences originally granted, 3 were surrendered (Vodafone M-Pesa, Aditya Birla, Tech Mahindra) citing non-viability. Now PPBL has been cancelled. This attrition rate raises questions about whether the current regulatory framework is calibrated correctly for a sustainable business model.

Way Forward / Reform Process

1. Raise or review the deposit ceiling

ForumIAS and industry experts recommend raising the ₹2 lakh ceiling further (or removing it for specific customer segments) to enable payments banks to build a larger float, improve income, and reduce cross-subsidisation needs. A tiered ceiling — higher for verified high-activity accounts — could balance inclusion with viability.

2. Introduce limited lending powers

Allow payments banks to offer small-ticket credit (micro-loans) based on transaction history data — a model already proven by digital lenders. This could be restricted to amounts under ₹50,000 with mandatory credit bureau reporting, creating a pathway to profitability while managing systemic risk.

3. Strengthen the KYC and compliance architecture

Mandate real-time KYC verification through Aadhaar-based e-KYC and AI-driven transaction monitoring. Require a “Chinese wall” between payments banks and parent group entities through independent board oversight, arm’s-length pricing, and ring-fenced technology infrastructure.

4. Revisit the SLR mandate for payments banks

The 75% G-sec requirement — designed for a universal bank’s risk profile — may be excessive for a payments-only institution. A differentiated SLR ratio (say 50–60%) could free up more earning assets without materially increasing systemic risk.

5. Pathway to Small Finance Bank status

Successful, compliant payments banks should have a clear, time-bound pathway to upgrade to Small Finance Bank (SFB) status — which allows lending. This “graduated licensing” approach already exists in principle but needs clearer milestones. Fino Payments Bank has explored this route.

6. Integrate with DBT and government schemes

India Post Payments Bank’s model — where DBT (Direct Benefit Transfers) flow directly into accounts — should be scaled. Routing MNREGA wages, PM-KISAN, and PM Awas Yojana payments through payments bank accounts ensures captive, regular deposits and builds customer relationships organically.

7. Supervisory technology (SupTech) for RBI

The Paytm case revealed that compliance gaps persisted for 8 years despite repeated RBI action. Real-time AI-powered monitoring of bank ledgers, KYC databases, and transaction patterns — as recommended by the 2024 Banking Sector Reforms discussion — would enable earlier, less disruptive intervention.

Global comparisons

The world’s most successful mobile money model. Operated by Safaricom (telecom), not a bank. Regulatory framework was iteratively built around the product rather than shoehorning a product into a pre-existing bank framework. Lesson: regulatory architecture must match the business model’s economics.

China allowed digital-only banks with full lending powers, backed by big-tech (Tencent/Alibaba). These have achieved massive scale and profitability by combining payments with data-driven credit. India’s prohibition on lending has prevented a similar trajectory for payments banks.

Fintech-bank hybrid under a “e-money issuer” licence. Offers a spectrum of services including micro-credit through partnerships. Demonstrates that the payments-credit integration can work with appropriate consumer protection safeguards.

Prelims Question

1. Payments Banks can invest up to 25% of their demand deposit balances in government and other approved securities (SLR-eligible assets).

2. Payments Banks are permitted to distribute insurance products of third-party companies but cannot issue credit cards.

3. A Scheduled Commercial Bank can take an equity stake in a Payments Bank under the Banking Regulation Act, 1949.

4. Payments Banks are excluded from the RBI’s Prompt Corrective Action (PCA) framework.

Which of the statements given above are correct?

Statement 1 — Incorrect: Payments Banks must invest at least 75%(not 25%) of their demand deposit balance in SLR-eligible government securities. The remaining 25% is to be deposited as time deposits with other scheduled commercial banks. This is a very commonly confused fact — UPSC frequently tests the inversion of this ratio.

Statement 2 — Correct: Payments Banks can distribute third-party financial products including insurance, mutual funds, and pension products. They are, however, explicitly prohibited from issuing credit cards (though debit cards are permitted).

Statement 3 — Correct: Under RBI’s payments bank guidelines, a promoter can have a tie-up with an existing scheduled commercial bank, and SCBs can take an equity stake in a Payments Bank. For example, Kotak Mahindra Bank holds a stake in Airtel Payments Bank; SBI holds a stake in Jio Payments Bank.

Statement 4 — Correct: The RBI revised its Prompt Corrective Action framework in January 2022, explicitly removing payments banks and small finance banks from the list of institutions subject to PCA. This is a high-yield UPSC fact tested in the context of banking regulation.

Mains questions

- India’s Push Beyond E20 Fuel: Reasons, Pitfalls, and the Flex Fuel Future - June 15, 2026

- RBI’s Reviving of FCNR(B) Swap Scheme again in 2026 - June 15, 2026

- Modi’s France Visit & the 52nd G7 Summit - June 13, 2026

No Comments