Overview of India Textile Sector

1. The Indian textile sector is one of the oldest industries in the country, dating back several centuries.It contributes about 2.3% to India’s GDP and 12% to export earnings (Economic Survey 2022-23).The industry employs over 45 million people directly and around 100 million indirectly (IBEF Report 2023).For example, cities like Tirupur and Surat thrive solely on textile-based employment.

2. India is the second-largest producer of textiles and garments globally, after China.

The global market share of Indian textiles stands at approximately 4%, according to WTO data.The country’s capability in producing a wide variety of fibers and yarns makes it globally competitive.According to a McKinsey report, India’s cotton yarn exports grew by 13% in 2022, supporting global supply chains.

3. The textile industry comprises both organized and unorganized sectors.

While large mills operate in the organized sector, handloom and handicrafts dominate the informal segment. According to the Ministry of Textiles, the unorganized sector contributes nearly 70% of production volume.

For instance, the Chanderi weaving cluster in Madhya Pradesh operates largely through traditional looms.

4. The industry is vertically integrated, covering the entire value chain from fiber to apparel.

This includes ginning, spinning, weaving, dyeing, and garment production, promoting self-reliance.The Cotton Corporation of India plays a crucial role in stabilizing cotton prices and supply. A 2022 report from CRISIL shows that vertical integration improved margins for large textile firms by 15%.

5. India is a hub for natural fiber-based textiles, particularly cotton.Cotton accounts for around 51% of the total textile production (Textile Ministry Annual Report 2022).

Its cultivation is prevalent in states like Maharashtra, Gujarat, and Punjab.In 2022, Maharashtra alone produced over 8 million bales of cotton.

6. The sector also has a significant presence in synthetic fibers and blended textiles.Polyester and viscose are gaining traction due to their durability and affordability.

Reliance Industries is a major player in synthetic fiber production in India. The synthetic textiles market in India was valued at $12 billion in 2022 (ASSOCHAM report).

7. Textile exports are vital to India’s foreign exchange reserves. Total exports from the sector amounted to around $44.4 billion in FY 2022-23 (DGFT Data).Major export destinations include the US, EU, UAE, and Bangladesh.For instance, apparel exports to the US alone accounted for $8.3 billion in 2022.

8. The industry is a key player in empowering women and rural artisans.Over 70% of handloom workers are women (National Handloom Census 2019). Initiatives like ‘India Handloom Brand’ promote traditional skills and products. In 2023, 80% of beneficiaries of the Handloom Marketing Assistance program were women.

Textile Sector Basket – Cotton, Jute, Woolen

1. Cotton Industry: India is the largest producer of cotton globally, contributing 23% of world cotton production. As per the Cotton Advisory Board, cotton output reached 36 million bales in 2022-23. Gujarat and Maharashtra are the leading cotton-producing states. For example, Gujarat accounted for 28% of national production in FY23.

2. Cotton textiles form the backbone of the Indian textile export market. Products like bedsheets, shirts, and denim have significant demand globally. The US and EU are major importers of Indian cotton garments.Cotton shirt exports to the US alone were valued at $1.1 billion in 2022.

3. Jute Industry: India is the largest producer of raw jute and jute goods, with West Bengal being the major hub. The jute industry supports around 4 lakh workers and 40 lakh farmers.

India produces nearly 1.7 million tonnes of raw jute annually (NJB Report 2023). For example, the Raghunathganj belt in Murshidabad specializes in jute sacks.

4. Jute is increasingly gaining traction due to eco-friendly demand. Products such as jute bags and carpets are promoted under “Plastic-free India” initiatives. The Ministry of Environment has supported jute packaging to reduce plastic usage. In 2023, the government made jute packaging mandatory for 100% of food grains.

5. Woolen Industry: Concentrated in northern India, especially Punjab and Himachal Pradesh. Ludhiana is known as the “Manchester of India” for woolen wear. India imports high-quality raw wool from Australia and New Zealand.For example, 95% of India’s fine wool comes from these imports (Wool Federation 2022).

6. Woolen textiles cater largely to domestic winterwear demand. Blankets, sweaters, and shawls are some common products. The Khadi and Village Industries Commission (KVIC) supports wool-based rural industries. In 2022, KVIC sold Rs 145 crore worth of woolen products.

7. Wool production in India is limited, and domestic sheep breeds provide coarse wool. The annual wool production is about 40 million kg, insufficient for the entire industry. Hence, India remains dependent on wool imports for quality garments. For example, Ladakh produces Pashmina wool, but in limited volumes.

8. The textile basket also includes technical textiles, silk, and man-made fibers.Technical textiles account for nearly 13% of total textile exports (FICCI Report 2023).Silk production is significant in Karnataka and Assam. India is the second-largest producer of silk globally, with over 35,000 MT output in 2022.

Impact of Make in India on Textile Industry

1. The ‘Make in India’ initiative has reinvigorated interest in domestic manufacturing. It has encouraged FDI and large-scale investments in textile parks. For instance, Arvind Ltd. and Welspun have expanded facilities under this push. Welspun invested Rs 2,000 crore in a smart textile park in Gujarat in 2022.

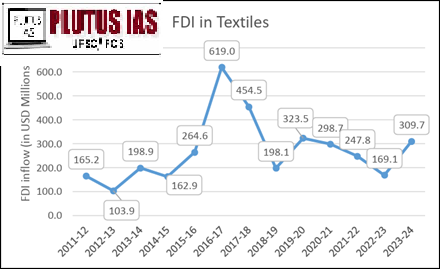

2. The scheme promotes local sourcing and self-reliance in textile production.Reduced dependence on Chinese imports has enhanced India’s global standing.According to DPIIT, India’s textile FDI inflow was $4.4 billion between 2000–2022.Local spinning mills have increased yarn capacity by 10% post-2020.

3. Infrastructure development under the initiative has boosted the sector. The setting up of Mega Textile Parks is an example of cluster-based growth. PM MITRA parks aim to create world-class industrial infrastructure. The first PM MITRA park was launched in Tamil Nadu in 2023 with a Rs 4,500 crore outlay.

4. It has led to enhanced employment opportunities across regions. The Textiles Ministry estimates that 1 lakh direct jobs were created under Make in India. Skill India has trained over 11 lakh workers in the apparel sector. In Odisha, over 10,000 artisans were trained in handloom skills under this mission.

5. Local artisans and MSMEs are integrated into the national supply chain. Initiatives like One District One Product (ODOP) benefit traditional textile clusters. For example, Bhagalpur silk and Banarasi sarees gained national promotion. ODOP reports show that handloom exports from Varanasi rose by 25% in FY23.

6. Export competitiveness has improved due to enhanced compliance and branding. ‘India Handloom Brand’ ensures quality assurance and market access. The Indian garment sector is now better aligned with global fashion trends. In 2022, Indian textile brands signed contracts with global retailers like H&M and Zara.

7. New technologies and automation were adopted under this initiative.Textile mills now utilize AI-based quality control and digital printing tech. Investment in R&D rose by 30% in key textile hubs like Surat and Tirupur. Example: Raymond Ltd. launched a smart fabric line with anti-viral properties.

8. Make in India has helped position India as an emerging textile hub. India was ranked among the top three textile manufacturing destinations globally (McKinsey Report 2022). The country aims to double its textile exports to $100 billion by 2030. As per Texprocil, export orders from EU brands grew by 18% in 2023.

Government Initiatives to Promote Textile Industry

1. PM MITRA (Mega Integrated Textile Region and Apparel) Parks: Launched to boost integrated textile value chains across 7 states. Each park is expected to attract Rs 10,000 crore investment and create 1 lakh jobs. The Tamil Nadu park already signed MoUs with 13 textile firms in 2023.

2. Production Linked Incentive (PLI) Scheme: Offers incentives for high-value MMF and technical textile production. Rs 10,683 crore has been allocated, expecting $20 billion in additional output. In FY23, 64 companies qualified for incentives under PLI for textiles.

3. National Technical Textiles Mission: Aims to increase India’s share in global technical textiles to 10% by 2025. Rs 1,480 crore is set aside for R&D and capacity building. In 2023, 40 new technical textile startups were incubated under the mission.

4. Skill India and SAMARTH schemes: Provide skill training to youth in apparel and textile operations. Over 13 lakh people trained under SAMARTH since its inception in 2017. States like Andhra Pradesh and Tamil Nadu lead in certified textile trainees.

5. Amended Technology Upgradation Fund Scheme (ATUFS): Supports modernization of textile machinery and infrastructure. Rs 17,822 crore worth of investment mobilized under ATUFS till 2023. Around 10,000 units benefited from machinery upgradation support.

6. Export Promotion Measures: Includes RoDTEP, RoSCTL, and duty drawback benefits for exporters. Apparel exports to the US rose by 20% post-extension of RoSCTL in 2022. RoDTEP covered 1,000+ textile HS codes in 2023 to ensure cost competitiveness.

7. Handloom and Handicraft Development Programs: National Handloom Development Program supports design and marketing. Over 1.5 lakh artisans benefitted under the Handicraft Mega Cluster scheme. For instance, the Kullu shawl cluster in Himachal Pradesh received Rs 22 crore in 2022.

Challenges Faced by the Indian Textile Sector

1. Infrastructure Gaps and High Logistics Costs: Inadequate warehousing, port connectivity, and inland transport raise production costs. According to the Ministry of Commerce, logistics costs account for 13–14% of textile exports versus the global average of 8–9%.

2. Fragmented and Unorganized Nature: A large portion of the sector is still unorganized, leading to inconsistent quality and lack of economies of scale. As per the Textile Committee 2022 report, over 70% of textile units are micro or small enterprises lacking formal financing.

3. Global Competition and Pricing Pressure: Countries like Bangladesh and Vietnam offer lower labor costs and better export incentives.For instance, India’s average unit price of garment exports is 15–20% higher than Bangladesh, affecting competitiveness.

4. Technology Obsolescence: Many units still use outdated machinery, reducing productivity and fabric quality. A CITI survey in 2023 revealed that only 38% of spinning mills use modern machinery with AI/automation.

5. Environmental Concerns and Sustainability: High water consumption and chemical effluents in dyeing units raise environmental alarms. According to CPCB, the textile sector is the second-largest industrial polluter of water bodies in India.

6. Raw Material Volatility: Cotton price fluctuations and dependency on imported wool impact production planning. For example, cotton prices surged by 40% in 2022 due to erratic monsoons and global supply chain issues.

7. Skilling and Labor Productivity Issues: Despite employment potential, many workers lack formal training in modern techniques. As per NSDC, 60% of textile workers are semi-skilled or unskilled, affecting efficiency.

8. Bureaucratic Hurdles and Compliance Load: Multiple licenses, GST complications, and frequent policy changes deter small-scale manufacturers. A FICCI report flagged that MSMEs spend nearly 18 days annually on compliance-related paperwork alone.

Way Forward

1. Strengthening Infrastructure and Cluster Development: Accelerate completion of PM MITRA parks and improve multimodal connectivity to reduce logistics costs. Adopt smart infrastructure and green buildings to promote sustainability.

2. Modernizing Machinery and Promoting R&D: Expand ATUFS and PLI coverage to include mid-sized enterprises for wider technology adoption. Establish more textile innovation hubs in collaboration with IITs and NIFT.

3. Promoting Sustainable and Circular Textiles: Incentivize eco-friendly processes and use of organic fibers through green certifications. Develop waterless dyeing and biodegradable fiber technologies.

4. Skill Development with Industry Collaboration: Deepen industry-academia tie-ups for demand-driven skilling programs. Introduce apprenticeship-led training to improve productivity at the grassroots level.

5. Enhancing Export Competitiveness: Negotiate favorable trade agreements like India-EU FTA to access larger markets. Simplify GST refund mechanisms and expedite RoDTEP reimbursements for MSMEs.

6. Empowering Handloom and Traditional Clusters: Digitize supply chains of rural artisans and integrate them into e-commerce platforms. Use Geographical Indications (GI) and branding to boost exports of niche products.

7. Encouraging FDI and Joint Ventures: Attract foreign textile brands to set up sourcing and production bases in India. Example: Encourage collaborations similar to the Aditya Birla-Zara alliance for fast fashion.

Conclusion

The Indian textile sector, with its vast diversity, rich heritage, and skilled manpower, holds the promise of becoming a global textile powerhouse. While it has significantly benefitted from initiatives like Make in India, PM MITRA, and PLI schemes, persistent structural and operational challenges need resolution. By modernizing infrastructure, enhancing sustainability, and empowering both artisans and entrepreneurs, India can achieve its vision of doubling textile exports and creating millions of jobs. Strategic reforms and inclusive growth will be key to positioning India not just as the world’s supplier but as a global trendsetter in textiles.

Prelims Questions

No Comments