06 Feb Ease of Doing Business: India’s Ongoing Regulatory Transformation

This article covers “Daily Current Affairs” and From Ease of Doing Business: India’s Ongoing Regulatory Transformation

SYLLABUS MAPPING

GS-3- Indian Economy – Ease of Doing Business: India’s Ongoing Regulatory Transformation

FOR PRELIMS

What key reforms in the Union Budget 2026–27 aim to improve Ease of Doing Business in India?

FOR MAINS

How has GST 2.0 strengthened Ease of Doing Business in India?

Why in the News?

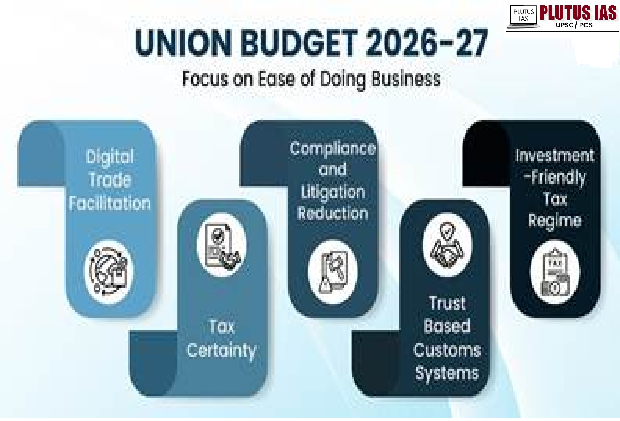

Ease of Doing Business (EoDB) is a key pillar of India’s economic reform strategy and growth agenda. The Union Budget 2026–27 emphasizes digital trade facilitation, tax certainty, reduced compliance and litigation, trust-based customs, and an investment-friendly tax regime. These reforms build on a decade of regulatory improvements aimed at simplifying procedures, enhancing transparency, and strengthening investor confidence.

Their impact is evident in rising investment and business activity. India attracted USD 748.38 billion in FDI between 2014 and 2025, a 143 percent increase over the previous period. Active registered companies also grew from 1.55 lakh in 2020–21 to 1.98 lakh in 2025–26, a 27 percent rise. Continued EoDB reforms, aligned with the Viksit Bharat @2047 vision, will support global value chain integration and industry-led growth.

Budget Focus on Ease of Doing Business

The Union Budget 2026–27 strengthens India’s Ease of Doing Business framework by improving tax certainty, reducing compliance burden, and promoting trust-based governance. Key reforms include rationalisation of Minimum Alternate Tax (MAT), simplification of dispute resolution mechanisms, and decriminalisation of minor procedural offences.

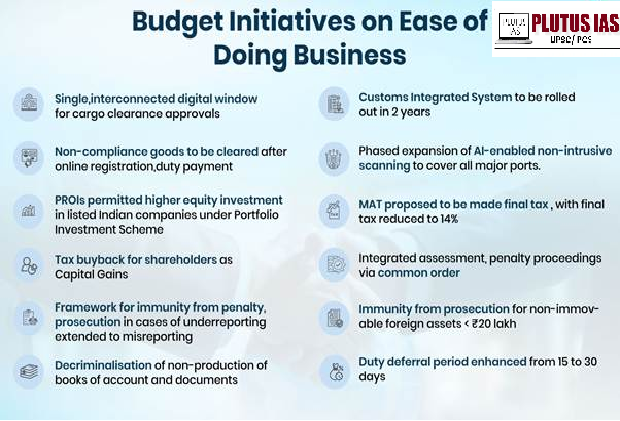

The Budget also introduces digital customs and logistics reforms through integrated digital systems and risk-based clearance mechanisms. These reforms aim to reduce transaction costs, improve operational efficiency, and make business processes faster and more transparent.

Rationalisation of Penalties and Prosecution

The Budget simplifies penalty and prosecution procedures by introducing integrated assessment and penalty proceedings through a single order. Interest on penalties during appeals will not be charged, and pre-payment requirements have been reduced from 20 percent to 10 percent.

Taxpayers will be allowed to update their returns even after reassessment proceedings by paying an additional 10 percent tax. The framework for immunity from penalties and prosecution has been extended to include cases of misreporting, provided the required additional tax is paid.

Minor offences such as non-production of books of accounts and certain TDS compliance requirements will be decriminalised and replaced with monetary penalties. Technical defaults will be treated as fee-based violations rather than criminal offences. Remaining prosecutions will be graded based on the severity of the offence, with imprisonment limited to two years and provisions for converting imprisonment into fines.

Immunity from prosecution has also been granted retrospectively from October 1, 2024, for non-immovable foreign assets below ₹20 lakh.

Trust-Based Customs Systems

The duty deferral period for Tier 2 and Tier 3 Authorised Economic Operators (AEOs) has been increased from 15 days to 30 days. This system allows businesses to clear imported goods first and pay customs duty later. This mechanism improves working capital management and supports just-in-time manufacturing.

Eligible manufacturer-importers will also receive the same duty deferral benefits. The validity period of advance rulings issued by customs authorities has been extended from three years to five years, providing greater certainty and improving business planning.

Trusted importers will receive preferential treatment, reduced inspections, and faster cargo clearance. Electronically sealed export cargo will be cleared directly from factory to ship. Customs warehousing systems will shift to operator-centric models using self-declarations, electronic tracking, and risk-based audits, reducing compliance burden and delays.

National Single Window System (NSWS)

The National Single Window System provides a digital platform for business approvals. It integrates approvals from 32 central departments and 32 state governments. It provides access to over 698 central and 7,435 state approvals.

Since its launch, the system has granted more than 8,29,750 approvals. It improves efficiency, transparency, and reduces approval timelines.

Other Digital Platforms

The PARIVESH 3.0 platform supports environmental clearance and compliance monitoring through integrated data systems and AI-based tools.

The e-Gram SWARAJ portal provides complete digital profiles of Gram Panchayats and improves transparency in local governance and development planning.

State-Level Reforms

States and Union Territories have removed more than 47,000 compliance requirements through simplification, digitisation, and decriminalisation.

States have simplified land use approvals, building regulations, labour laws, and environmental clearances. Self-certification and third-party approvals have reduced delays and improved efficiency.

These reforms have improved investment implementation and business efficiency.

Business Reforms Action Plan (BRAP)

The Business Reforms Action Plan has been implemented since 2015 to improve regulatory transparency and simplify procedures. The eighth edition, BRAP 2026, continues to strengthen reforms at state and district levels.

States such as Kerala, Tamil Nadu, and Andhra Pradesh have introduced digital approvals, land reforms, and streamlined industrial approval systems.

Structural and Financial Reforms

Structural reforms have focused on regulatory simplification, institutional consolidation, and technology-driven governance across financial markets, taxation, labour, banking, and environmental regulation. Reforms in insurance, securities, GST, labour codes, and public sector banking aim to reduce compliance burdens, enhance transparency, improve access to finance, strengthen regulatory certainty, and promote competition, creating a more efficient and resilient business ecosystem.

Regulatory Measures

The Reserve Bank of India reorganised its regulatory framework by consolidating over 9,000 circulars into 238 function-specific Master Directions. Out of 9,446 circulars, 3,809 have been subsumed and 5,673 deemed obsolete, improving regulatory clarity and reducing compliance burdens to enhance EoDB.

Sabka Bima Sabki Raksha (Insurance Reforms)

The 2025 Amendment to insurance laws revised the Insurance Act, LIC Act, and IRDAI Act to improve citizen protection, deepen insurance penetration, and facilitate sector growth. Key measures include allowing up to 100% FDI in insurance companies, one-time registration for intermediaries, raising limits for IRDAI approval on equity transfers from 1% to 5%, and reducing Net Owned Funds requirement for foreign reinsurers from ₹5,000 crore to ₹1,000 crore. The Indian Insurance Companies (Foreign Investment) Amendment Rules, 2025 further rationalise conditions for insurers and intermediaries.

Credit Assessment Model (CAM)

Launched by public sector banks in 2025, CAM uses digital footprints to assess MSME credit. Between April and December 2025, over 3.96 lakh MSME loans worth ₹52,300 crore were sanctioned. The model improves EoDB by enabling automated loan appraisal, objective decision-making for all applications, model-based limit assessment for both new and existing MSME borrowers, and integration with credit guarantee schemes.

Labour Reforms

The consolidation of 29 Central labour laws into four Labour Codes has significantly enhanced Ease of Doing Business by simplifying compliance, reducing approval timelines, and providing greater operational flexibility, particularly for MSMEs.

The Codes have prescribed a 30-day time limit for granting permission for factory construction or expansion and reduced the overall approval timeline from 90 days to 30 days.

They simplify contract labour norms by exempting contractors employing fewer than 50 workers from licensing, and introduced electronic single registration, a single return, and single all-India licences valid for five years with deemed approvals.

The Codes replaced six existing boards with a single national tripartite board, enabled compounding of offences through graded monetary fines, replaced criminal penalties with civil penalties, and mandated a 30-day notice period for compliance before legal action.

They also increased thresholds for lay-off, retrenchment, closure, and Standing Orders to 300 workers, providing greater operational flexibility to establishments without prior approvals.

GST 2.0

GST reforms introduced in September 2025 strengthen Ease of Doing Business by simplifying tax slabs, reducing rates across key sectors, thus lowering tax incidence and improving price competitiveness. The move towards a simplified two-rate structure lowers compliance and transaction costs, while rate rationalisation improves affordability and supports entrepreneurship.

The impact is reflected in the expansion of the tax base, with registered taxpayers increasing from about 60 lakhs in 2017 to over 1.5 crore in November 2025, indicating deeper formalisation. Further, correction of inverted duty structures in labour-intensive and agri-input sectors such as textiles and fertilisers has reduced costs and working capital pressures, easing business operations.

Conclusion

India’s Ease of Doing Business environment continues to improve through regulatory simplification, digitalisation, and trust-based governance. The Union Budget 2026–27 strengthens tax certainty, reduces compliance burden, and promotes investment.

These reforms have increased investment, business growth, and economic formalisation. They will continue to strengthen India’s competitiveness and support long-term economic development under the Viksit Bharat @2047 vision.

Best ias coaching in delhi Best ias coaching in chandigar

Prelims question:

Which of the following measures introduced in Union Budget 2026–27 aim to improve Ease of Doing Business in India?

1.Rationalisation of Minimum Alternate Tax (MAT)

2.Digital customs and risk-based clearance systems

3.Consolidation of 29 Central labour laws into 4 Labour Codes

4.Increase in FDI limit for insurance companies to 100%

Select the correct answer:

A) 1 and 2 only

B) 2, 3 and 4 only

C) 1, 2, 3 and 4

D) 1 and 3 only

Answer: C

Q. “Examine how the Union Budget 2026–27 strengthens Ease of Doing Business in India and its potential impact on investment and economic growth.” (250 words)

- Artemis II: Humanity’s Return to Lunar Space and India’s Place in the New Moon Race - April 2, 2026

- A Missed Opportunity to Guarantee Minimum Wages - March 31, 2026

- ‘India’s Growth Claims, A Clash with Data Reality’. - March 30, 2026

No Comments