11 Mar Kisan Credit Card: Fueling Growth in Agriculture and Strengthening Farmers’ Access to Capital.

This article covers “Daily Current Affairs” and From Kisan Credit Card: Fueling Growth in Agriculture and Strengthening Farmers’ Access to Capital.

SYLLABUS MAPPING

GS- 3 – Agriculture, Inclusive Growth, and Rural Economy – Kisan Credit Card: Fueling Growth in Agriculture and Strengthening Farmers’ Access to Capital.

FOR PRELIMS

Discuss the key features of the Kisan Credit Card scheme.

FOR MAINS

Institutional credit plays a crucial role in enhancing agricultural productivity in India.

Why in the news?

Recently, the Kisan Credit Card (KCC) scheme has taken centre stage in India’s agricultural policy discourse due to its massive scale and recent digital transformations. The scheme has reached a significant milestone with over 7.72 crore active KCCs nationwide, facilitating an outstanding credit flow of approximately Rs. 10.2 lakh crore. The government has recently enhanced the financial safety net for farmers by increasing the collateral-free loan limit to Rs. 2 lakh and raising the overall crop loan limit under the Modified Interest Subvention Scheme (MISS) to Rs. 5 lakh. Furthermore, the successful integration of the Kisan Rin Portal (KRP) and the ongoing KCC Saturation Drive under Atmanirbhar Bharat have brought the scheme into the spotlight as a primary engine for rural financial inclusion and agricultural modernization.

About Kisan Credit Card (KCC) scheme.

Institutional credit serves as the lifeblood of Indian agriculture, a sector that remains the backbone of the national economy. With approximately 46.1 per cent of the Indian population dependent on agriculture and allied activities for their livelihoods, ensuring a steady, affordable, and timely flow of capital is essential for national food security and rural stability. Without access to formal credit, farmers often fall into the trap of informal moneylenders who charge exorbitant interest rates, leading to a cycle of debt and poverty.

To address these systemic challenges, the Government of India introduced and subsequently modernized the Kisan Credit Card (KCC) scheme. The primary objective of the KCC is to provide a single-window credit delivery system that offers farmers adequate and timely support for their requirements. This includes short-term credit for crop cultivation, post-harvest expenses, and even investment credit for allied activities like animal husbandry and fisheries. By streamlining the lending process, the KCC aims to empower farmers with the financial flexibility needed to manage their production cycles efficiently and transition toward more productive farming practices.

Background and Evolution of Kisan Credit Card Scheme

The Kisan Credit Card Scheme was launched in 1998 with the visionary goal of simplifying the way farmers accessed short-term institutional credit. Initially, the scheme focused almost exclusively on crop production, helping farmers purchase inputs like seeds and fertilizers. It was implemented through a robust network involving NABARD (National Bank for Agriculture and Rural Development) and a variety of banking institutions, including Commercial Banks, Regional Rural Banks (RRBs), and Cooperative Banks.

Over the decades, the scheme has undergone significant evolution to meet the changing needs of the agrarian economy. A major milestone occurred in 2006–07 with the launch of the Interest Subvention Scheme (now MISS), which made credit significantly more affordable. The most transformative shifts, however, have occurred recently. In 2018–19, the government expanded the KCC facility to include fishers and fish farmers to meet their working capital needs. This was followed by the Revised Kisan Credit Card (2020) scheme, which adopted a more holistic approach. It moved beyond simple transaction-based lending to provide integrated support for cultivation, allied activities, and even household consumption needs. Today, the scheme is supported by a diversified delivery architecture involving 457 onboarded banks, ensuring that credit reaches the grassroots level across all Indian states.

Key Features of the Kisan Credit Card Scheme

The KCC scheme is defined by its farmer-centric features designed to remove traditional barriers to formal finance.

Simplified Credit Access: The government has introduced a simplified one-page application form. To further ease the process, many details are pre-filled using records from the PM-KISAN portal, requiring farmers to only provide land records and crop information.

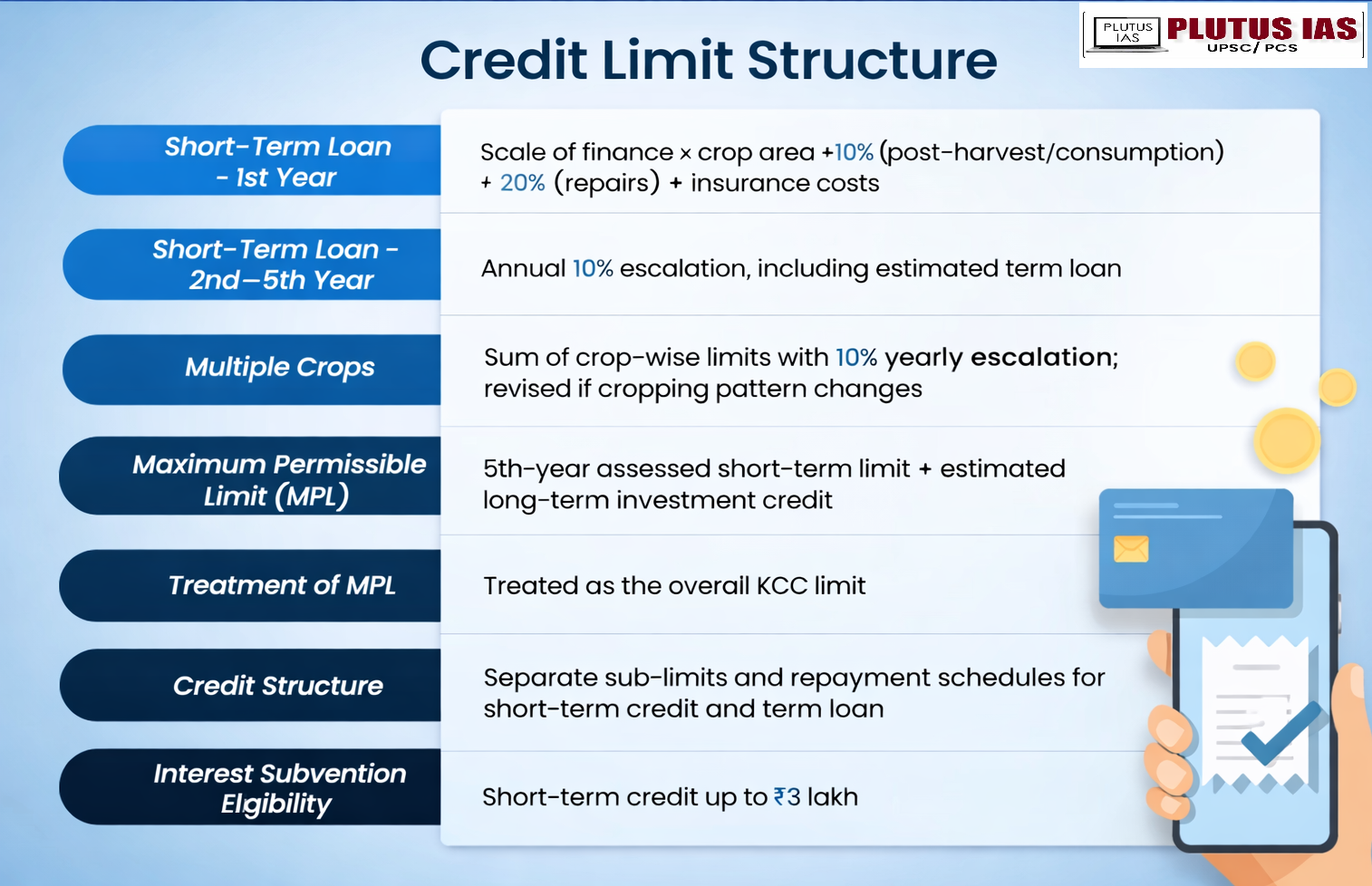

Flexible Repayment and Structure: The KCC offers a revolving credit facility with a validity of up to five years. This allows farmers to withdraw and repay funds as per their production cycles and cash flows.

Interest Subvention Benefits: Under MISS, farmers can access short-term loans up to Rs. 3 lakh at a base interest rate of 7%. For those who repay on time, an additional 3% subvention is provided, bringing the effective interest rate down to just 4%.

Broad Coverage: The scheme provides a composite credit limit. For marginal farmers, this limit (ranging from Rs. 10,000 to Rs. 50,000) covers post-harvest requirements, consumption expenses, and small investments independent of land valuation.

Digital Integration: The modern KCC is RuPay-enabled, facilitating digital payments and reducing cash dependence. Additionally, the Kisan Rin Portal (KRP) serves as a unified digital platform that integrates farmer profiles and loan disbursement data, ensuring transparency in interest subvention claims.

Role of KCC in Strengthening Agricultural Growth

The KCC scheme has become a cornerstone of agricultural productivity and financial resilience in India. By providing affordable institutional credit, it allows farmers to invest in high-quality seeds, fertilizers, and modern farm equipment, which directly leads to improved yields and higher incomes.

One of the most significant impacts of the KCC is the reduction of dependence on informal moneylenders. By offering collateral-free loans up to Rs. 2 lakh, the scheme has significantly reduced entry barriers for the most vulnerable. It plays a vital role in the financial inclusion of small and marginal farmers, who currently hold approximately 76 percent of all agricultural credit accounts.

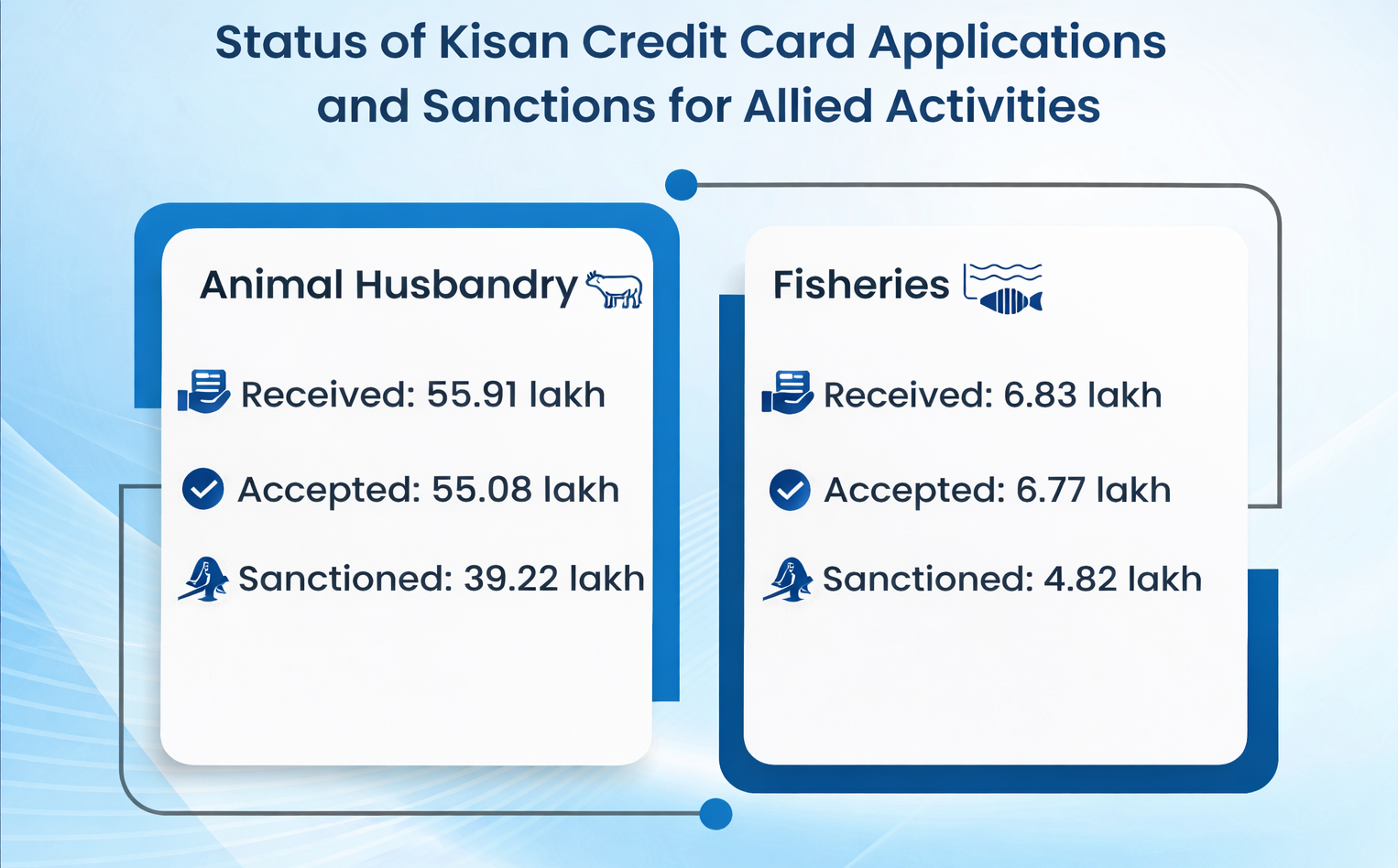

Furthermore, the expansion of the KCC to allied sectors has diversified rural income streams. In the animal husbandry sector, for example, the scheme saw an exceptionally high acceptance rate, with 39.22 lakh applications sanctioned out of 55.9 lakh received. In the fisheries sector, 4.82 lakh applications have been sanctioned, indicating a successful conversion of demand into actual financial support for fish farmers.

Finally, the KCC acts as a tool for risk management. In the event of natural calamities, the scheme allows for interest-free periods of up to one year, which can be extended to five years in cases of severe disasters. This flexibility enhances the financial resilience of farmers against climate-related and market risks, contributing to long-term sectoral stability.

Challenges and Limitations

Despite its successes, the KCC scheme faces several hurdles that prevent it from reaching its full potential. While the government has launched extensive IEC (Information, Education, and Communication) campaigns, low awareness remains a challenge in remote regions where farmers may not fully understand the digital components or the subvention benefits.

A critical limitation is the reach among tenant farmers, oral lessees, and sharecroppers. Although the scheme officially includes them, these groups often struggle to provide the necessary land documentation or lack the formal recognition required by some bank branches. This leads to regional disparities, where states with better land record digitization show much higher KCC penetration than those lagging behind.

Procedural delays can also occur at the branch level. While the central government has simplified the form to a single page, some banks may still require additional documentation, leading to friction in the application process. Additionally, there are ongoing concerns regarding loan misuse, where credit intended for agricultural production might be diverted to non-productive household consumption, potentially leading to over-indebtedness if not monitored carefully. While the KCC provides for consumption needs, balancing this with production goals is a constant challenge for credit administrators.

Government Initiatives and Recent Measures

The Government of India has been proactive in addressing the gaps in the KCC framework through several high-impact initiatives.

KCC Saturation Drives: Under the Atmanirbhar Bharat Abhiyan, the government conducts nationwide drives to ensure every eligible farmer is covered. These drives include weekly district-level camps specifically targeting those in animal husbandry and fisheries.

Digitization via Kisan Rin Portal: Launched in September 2023, the Kisan Rin Portal (KRP) has revolutionized KCC implementation. It enables automated processing of interest subvention claims, reducing settlement delays and enhancing transparency for both banks and farmers.

PM-KISAN Linkage: The KCC application process has been integrated with the PM-KISAN portal, allowing banks to use existing verified data to speed up the onboarding of new borrowers.

Enhanced Limits: For the 2025–26 period, the government significantly increased lending limits. The crop loan limit under MISS rose from Rs. 3 lakh to Rs. 5 lakh, and the fisheries limit similarly increased to Rs. 5 lakh, reflecting a strong policy commitment to the allied sectors.

Way Forward

To further strengthen the KCC framework, several reforms could be implemented. First, there must be a concerted effort to expand access for tenant farmers and sharecroppers by moving toward a “cultivator-based” identification system rather than a strictly “owner-based” one. This could involve leveraging Farmer Producer Organizations (FPOs) to act as intermediaries for credit delivery.

Second, the integration of fintech and digital credit delivery should be accelerated. While the Kisan Rin Portal is a great start, further end-to-end digitization from application to disbursement can eliminate the remaining procedural delays. This should be coupled with strengthening financial literacy through grassroots outreach, ensuring farmers understand how to use RuPay cards and manage their revolving credit effectively.

Finally, better monitoring and targeted credit distribution are essential. Using data analytics from the Kisan Rin Portal, the government can identify regions with low penetration and deploy “mobile credit vans” or dedicated saturation camps to bridge the gap. Ensuring that credit is aligned with the specific cropping patterns and agro-climatic zones of each region will make the credit more “productive” and reduce the risk of over-indebtedness.

Conclusion

The Kisan Credit Card scheme has evolved from a simple credit tool into a robust financial ecosystem that supports the diverse needs of the Indian farmer. By providing affordable, timely, and flexible capital, it has not only increased agricultural productivity but also acted as a shield against the predatory practices of informal lenders. The recent digital reforms and the expansion into allied sectors like dairy and fisheries signify a shift toward a more inclusive and modern agrarian economy. As India strives for sustainable agricultural growth and rural prosperity, the continued strengthening of the KCC framework through digitization, saturation drives, and policy innovation will remain essential for achieving long-term agrarian stability and ensuring that no farmer is left behind in the journey toward a Viksit Bharat

Best ias coaching in delhi Best ias coaching in chandigar

Prelims question:

Q. With reference to the Kisan Credit Card (KCC) scheme, consider the following statements:

1.The scheme provides credit only to owner-cultivators, excluding tenant farmers and sharecroppers.

2.The collateral-free credit limit for KCC borrowers has been enhanced to Rs. 2 lakh effective from January 1, 2025.

3.Under the Modified Interest Subvention Scheme (MISS), the effective interest rate for farmers who repay on time is 4%.

4.The KCC facility was extended to fishers and fish farmers in the year 2018–19.

Which of the statements given above are correct?

(a) 1 and 2 only

(b) 2 and 3 only

(c) 2, 3, and 4 only

(d) 1, 2, 3, and 4

Answer: (c) 2, 3, and 4 only

Mains Question:

“The Kisan Credit Card (KCC) scheme has evolved from a transaction-based lending tool into a holistic financial instrument for rural India.” In this context, discuss the impact of recent digital interventions and the inclusion of allied sectors in strengthening the financial resilience of farmers. (250 words)

- Artemis II: Humanity’s Return to Lunar Space and India’s Place in the New Moon Race - April 2, 2026

- A Missed Opportunity to Guarantee Minimum Wages - March 31, 2026

- ‘India’s Growth Claims, A Clash with Data Reality’. - March 30, 2026

No Comments